Last updated: May 19, 2026

Startup funding trends in 2026 are defined by a strange split: more money is entering venture capital, but less of it feels available to the average founder. The headline numbers look generous. The market underneath them is much more selective.

According to Crunchbase’s Q1 2026 funding report, global startup investment hit about $300 billion in the first quarter of 2026, the highest quarter on record in its dataset. KPMG’s Venture Pulse put the quarter even higher at $330.9 billion across 8,464 deals, more than double Q4 2025 investment.

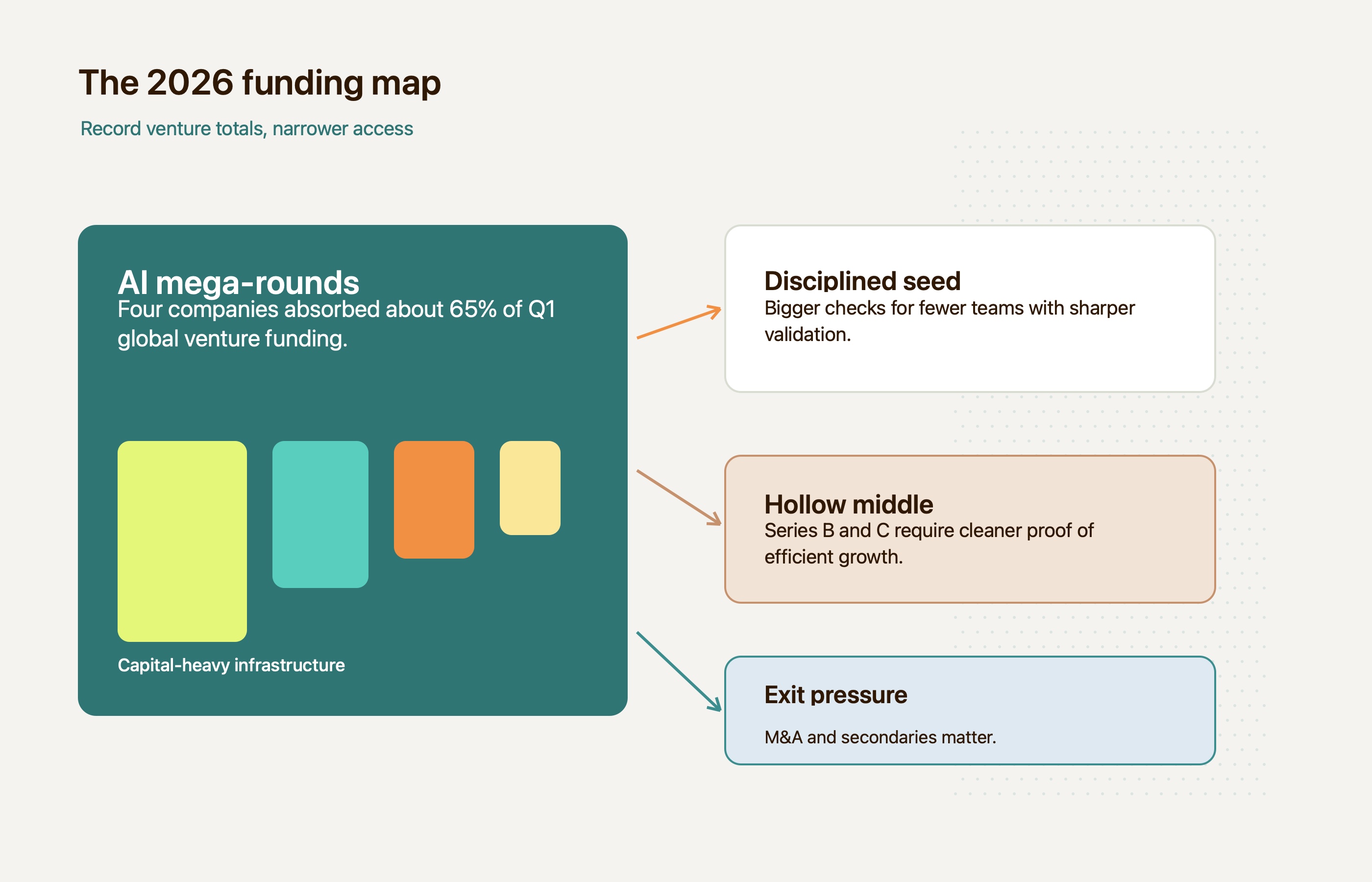

But that does not mean venture capital is back to 2021 behavior. The money is concentrated. Crunchbase reported that OpenAI, Anthropic, xAI, and Waymo raised a combined $188 billion, or roughly 65% of global venture funding in the quarter. AI companies captured $242 billion, or 80% of total global funding.

The practical lesson for founders is simple: 2026 is not a broad risk-on market. It is a conviction market. Investors are willing to write enormous checks when they believe a company owns infrastructure, distribution, data, or category-defining leverage. For everyone else, the funding bar is higher, the middle of the market is thinner, and the product must show evidence sooner. The UK startup ecosystem shows how this concentration plays out inside a major AI and fintech market.

The big startup funding trend in 2026 is concentration

The most important startup funding trend in 2026 is not just AI. It is capital concentration.

KPMG reported that ten funding rounds above $2 billion contributed more than $206 billion to Q1 2026’s global VC total. That is why a founder can read record-breaking venture headlines and still hear “come back with more traction” from investors.

Silicon Valley Bank described this as a barbell effect in venture capital: massive late-stage rounds at one end, disciplined early-stage investing at the other, and a thinner middle. SVB also noted that in 2025, 33% of all U.S. VC dollars went to the top 1% of companies by valuation, up from 12% in 2022.

That shift changes how founders should interpret market momentum. A rising funding total does not automatically mean more investor appetite for broad SaaS, consumer apps, or undifferentiated marketplaces. It can mean the opposite: mega-rounds are absorbing capital and attention while other founders compete for fewer conviction-based checks.

What concentration means for a startup raising now

If you are not building foundation models, data centers, chips, autonomous systems, or a similarly capital-intensive platform, the market is asking a different question: can this company become efficient before it becomes expensive?

Founders should expect investors to press harder on:

- Revenue quality, not just pipeline

- Retention, not just acquisition

- Gross margin and support burden

- Sales cycle length

- Payback period

- Product usage depth

- Founder-market fit

- Why the company needs venture capital instead of slower, revenue-funded growth

That is especially important before seed and Series A. An early product does not need every enterprise feature, but it does need to prove a real buying or usage behavior. Hapy’s guide to MVP development cost in 2026 makes the same point from the build side: the best early product budget buys evidence, not feature volume.

AI startup funding is moving from software to infrastructure

AI startup funding in 2026 is no longer just about chat interfaces or model wrappers. The largest checks are going into the physical and operational stack beneath AI: compute, data centers, semiconductors, energy, robotics, autonomous vehicles, and vertical workflows that can turn AI into measurable productivity.

Crunchbase reported that Q1 2026’s AI funding record was driven by frontier labs and infrastructure-heavy companies. KPMG’s Venture Pulse named OpenAI, Anthropic, xAI, Waymo, Databricks, Polymarket, and Shield AI among the largest U.S.-based AI-focused rounds in the quarter.

This matters because it changes what “AI startup” means to investors. Adding generative AI to an existing workflow is no longer enough. The stronger question is whether AI gives the company a durable edge:

- Does the product create proprietary workflow data?

- Does it automate a costly decision, not just assist with writing?

- Does it improve unit economics for customers?

- Does it reduce labor, cycle time, fraud, waste, or compliance risk?

- Does the architecture become more defensible as usage grows?

For founders, the strongest AI pitch in 2026 is not “we use AI.” It is “AI changes the economics of this workflow, and here is the evidence.”

Agentic AI and physical AI are becoming investable categories

The report’s strongest sector insight is that venture capital is moving toward agentic and physical AI.

Agentic AI refers to systems that can complete multi-step tasks with limited human intervention. In enterprise settings, that can mean AI agents handling financial operations, legal intake, customer support triage, procurement, clinical administration, or manufacturing workflows. Physical AI includes robotics, autonomous vehicles, aerospace, sensors, and other systems where software meets the physical world.

The investor logic is easy to understand. Pure software can be copied quickly. A vertical AI system connected to data, operations, compliance, hardware, or payments is harder to displace. It also creates clearer ROI for buyers because the product is tied to cost reduction or revenue throughput.

That is one reason the “SaaS-pocalypse” narrative keeps showing up in investor conversations. The weaker version is overblown: SaaS is not going away. The stronger version is useful: generic horizontal software is under pressure if AI can recreate features faster than companies can defend them. Founders building in this category should also know what SaaS product-market fit now has to prove before they pour money into sales.

We covered that strategic difference in vertical SaaS vs. horizontal SaaS. In the 2026 funding market, vertical depth is not just a product decision. It is a fundraising advantage, and it should still connect back to a durable SaaS business model.

The old funding ladder is harder to climb

The venture ladder used to feel more linear: raise pre-seed, build a product, raise seed, show traction, raise Series A, scale toward Series B. In 2026, that ladder has more missing rungs.

The report points to a hollowed-out Series B and C market. SVB’s broader framing supports the same conclusion: early investors still want pre-consensus companies, and late-stage capital still chases outliers, but the middle requires much stronger proof than it did during the easy-money period.

Crunchbase’s Q1 2026 data shows how nuanced the early market is. Seed funding reached $12 billion, up 31% year over year, but the increase came from larger rounds while seed deal count fell 30% year over year. Early-stage funding rose too, yet the competition for attention remains intense because investors are more selective about which teams deserve larger checks.

The result is a market where “we are growing” is too vague. Investors want to know what kind of growth:

| Funding stage | Weak signal in 2026 | Stronger signal in 2026 |

|---|---|---|

| Pre-seed | Big market, early deck, founder ambition | Specific problem, credible founder-market fit, sharp wedge, fast validation plan |

| Seed | Prototype, waitlist, broad feature roadmap | Working MVP, active users or pilots, clear activation behavior, early willingness to pay |

| Series A | Revenue growth without quality detail | Repeatable acquisition, retention, gross margin, usage depth, clear ICP |

| Series B/C | Expansion story built on spend | Efficient growth, scalable sales motion, strong unit economics, defensible product data |

That does not mean founders should overbuild before raising. It means the MVP has to be designed around the proof investors care about. If the next round depends on paid pilots, build the pilot workflow. If the next round depends on retention, build onboarding, analytics, and the core habit loop. If the next round depends on enterprise trust, budget for security, admin controls, and reliability early.

Venture capital is rewarding fundamentals again

The end of near-zero interest rates still hangs over startup funding in 2026. Even after rate cuts in 2025, the market is not behaving like capital is free. Limited partners are more cautious, venture funds are more concentrated, and founders are being pushed toward capital efficiency.

That macro environment explains why the same market can produce record AI rounds and tougher fundraising conversations for normal startups. When the cost of capital is higher, investors need a better reason to accept long-duration risk. The answer can be extraordinary scale potential, as with frontier AI, or it can be near-term efficiency and evidence, as with disciplined early-stage companies.

For founders, this shifts the fundraising story away from pure TAM and toward operating leverage:

- How does the product become cheaper to deliver over time?

- What part of the workflow becomes more automated?

- What data advantage compounds?

- What customer segment has the highest willingness to pay?

- Where does the product reduce headcount, delay, risk, or error?

This is where technical and product decisions become fundraising decisions. A bloated MVP with five half-proven workflows makes the company harder to explain. A narrow product that proves one expensive problem can make the company easier to fund.

For teams preparing to raise, Hapy’s MVP Readiness Check is built around that discipline: is the idea ready to build, or does the team need sharper evidence before spending heavily?

Regional funding is global, but the U.S. still dominates AI capital

The report’s regional data tells a clear story: capital is globalizing, but AI mega-rounds keep the U.S. at the center of venture gravity.

Crunchbase reported that U.S.-based startups raised $250 billion, or 83% of global venture capital in Q1 2026. KPMG’s dataset put U.S. investment at $267.2 billion in the same quarter. Both sources show the same pattern: the U.S. captured the overwhelming majority of capital because the largest AI and infrastructure companies are U.S.-based.

Europe and Asia are still moving, just differently.

KPMG reported that Europe rose to a 14-quarter high of $25.7 billion in Q1 2026, while Asia climbed to a 12-quarter high of $31.8 billion. The broader research also points to a European shift from consumer startups toward deep tech, defense, infrastructure, and frontier AI. The U.K. remains a leading hub, while France’s Mistral and other AI labs show that Europe can still produce globally relevant technical companies.

Asia’s story is more varied. China remains important in semiconductors, autonomous vehicles, and robotics. Southeast Asia saw funding improvement, but the report notes that a large Singapore data center deal distorted the regional total. India remains a major SaaS and fintech market, with Bengaluru continuing to climb as a startup ecosystem. Regional founders can compare those patterns with the startup ecosystem in Saudi Arabia when deciding whether to raise locally, sell cross-border, or build for a more specific market wedge.

For European go-to-market planning, the Germany startup ecosystem and Switzerland startup ecosystem guides break down where B2B SaaS, AI, fintech, healthtech, and enterprise software opportunities are more specific than the headline funding numbers.

Frontier markets matter, but capital gaps remain

For founders, operators, and investors working across the U.S., U.K., Australia, Europe, the Middle East, and emerging markets, the regional lesson is not to chase one geography. It is to understand where capital is concentrated, where talent is improving, and where underfunded markets can produce efficient companies. Our Middle East tech trends guide is a useful companion for that regional read.

Pakistan is one useful example from the research, not the whole audience. Business Recorder’s coverage of the inDrive and Dealroom report says Pakistan’s startup ecosystem now exceeds $4 billion in combined enterprise value, with startup formation accelerating across fintech, transportation, and marketing. It also notes that smartphone ownership reached roughly 68% in 2023-2024, while mobile broadband coverage extended to around 81%.

The opportunity is not that Pakistan is suddenly overfunded. It is the opposite. The same report cited by Business Recorder points to a meaningful capital gap, with startup funding around $57 million, far below regional peers. That gap can slow growth, but it can also create room for operator-led investors, cross-border customers, and efficient technical teams to build durable companies before valuations overheat.

The practical path for founders in undercapitalized ecosystems is not to mimic Silicon Valley’s capital intensity. It is to build for clear economic value: payments, logistics, healthcare access, B2B operations, exportable software services, and workflow automation where local insight becomes an advantage.

Sector signals: fintech, climate tech, life sciences, and hard tech

AI is the headline, but the report’s sector detail shows a broader investor preference for infrastructure and measurable utility.

Fintech is not back to speculative excess. It is becoming more selective. Innovate Finance reported that global fintech companies raised $53 billion across 5,918 deals in 2025, with the U.S. leading, the U.K. second, and India close behind. Its 2026 outlook highlights stablecoins, AI-native operations, B2B payments, compliance, treasury tooling, and embedded finance as key themes.

That fits the broader funding pattern. Investors are more interested in fintech that owns rails, risk, settlement, compliance, or business workflows than fintech that depends on expensive consumer acquisition.

Climate tech is moving in a similar direction. J.P. Morgan’s 2026 climate tech outlook points to energy resilience, grid reliability, advanced batteries, and infrastructure modernization. Software still matters, especially when AI helps optimize energy usage or environmental monitoring, but the capital is flowing toward physical systems that can change the economics of decarbonization.

Life sciences and healthcare are also behaving more selectively. The report describes targeted consolidation, stronger interest in defensible IP, and a biotech IPO window that is more open than broad software. In other words, investors are not avoiding risk. They are choosing risk with clearer moats.

The common thread across these sectors is not hype. It is defensibility plus measurable value.

Exits are improving, but liquidity is still uneven

Funding depends on exits because venture capital has to recycle capital. In 2026, that exit machine is partly moving again, but not evenly.

KPMG reported that global VC exit value rose to $413.5 billion in Q1 2026, the highest level since Q4 2021, driven mainly by large M&A while IPO activity remained more muted. Crunchbase also reported stronger startup M&A in Q1, with exits cumulatively valued above $56.6 billion in its dataset.

The IPO market is open, but selective. Crunchbase noted that PayPay was the largest venture-backed IPO in Q1 2026, with a $10 billion valuation on listing, while Chinese AI labs Z.ai and MiniMax also debuted in Hong Kong at valuations above $6 billion. Many U.S. companies remain cautious, especially if public investors would price them below peak private valuations.

That is why secondaries matter. The report notes that private secondary markets are becoming a liquidity valve for employees and early investors in companies that stay private longer. This does not solve the entire exit backlog, but it reduces pressure for some of the strongest private companies.

For founders, the implication is uncomfortable but useful: build a company that can survive multiple exit paths. A business that only works if the IPO window is perfect is fragile. A business with strategic buyer value, strong gross margins, customer concentration discipline, and clean data rooms has more options.

What founders should build before raising in 2026

The funding market is not closed. It is narrower. That means founders need to build the smallest credible proof for the next capital milestone.

Use this sequence before raising:

- Define the funding question. Are you proving demand, usage, revenue, margin, technical feasibility, or enterprise readiness?

- Choose one wedge. A narrow ICP and painful workflow are easier to fund than a broad platform story without evidence.

- Build the evidence path. The MVP should capture the behavior investors need to see: activation, payment, retention, productivity gain, or cost reduction.

- Track the right metrics early. Do not wait until fundraising to instrument the product.

- Show why the product gets stronger with use. Data, workflow depth, integrations, switching costs, and operational learning matter more in 2026.

- Keep post-launch runway. A version-one product without iteration budget is not capital efficient. It is a frozen bet.

The stronger founder narrative is no longer “this market is huge.” It is “this customer has an expensive problem, our product changes the economics of solving it, and early evidence shows the behavior is real.” That story also needs technical judgment; many early teams need a startup CTO or fractional technical lead before the first large funding round, not after the architecture has already drifted.

That is also how we think about MVP development at Hapy Co. Version one should not be a miniature enterprise platform. It should be a focused system for learning, selling, and proving the next step.

The founder takeaway

Startup funding trends 2026 point to a market with more capital and less patience.

AI infrastructure, agentic systems, autonomous platforms, fintech rails, climate hard tech, and defensible vertical software can still attract serious capital. But for most founders, the investor conversation has moved from possibility to proof.

The best response is not to chase every hot sector label. It is to build a product that makes one valuable workflow measurably better, then use that evidence to raise from a position of clarity.

If you are preparing to raise this year, the question is not only whether your market is fundable. It is whether your product is built to produce the evidence this funding market now demands.

FAQ

What are the biggest startup funding trends in 2026?

The biggest startup funding trends in 2026 are record AI mega-rounds, capital concentration in a small number of category-leading companies, tougher mid-stage fundraising, more disciplined seed investing, stronger M&A activity, and growing use of secondary markets for liquidity.

Why is AI startup funding so high in 2026?

AI startup funding is high because the category now includes capital-intensive infrastructure: foundation models, data centers, semiconductors, energy systems, autonomous vehicles, robotics, and vertical AI workflows. These companies often need far more capital than traditional software startups.

Is 2026 a good year to raise venture capital?

2026 can be a good year to raise venture capital if the company has strong evidence, a clear market wedge, efficient growth, and a credible reason to scale quickly. It is harder for startups with broad stories, weak usage, unclear unit economics, or features that AI can easily copy.

Which startup sectors are investors watching in 2026?

Investors are watching AI infrastructure, agentic AI, physical AI, fintech infrastructure, stablecoin payments, cybersecurity, climate hard tech, energy resilience, healthcare IP, robotics, autonomous systems, and vertical SaaS with measurable efficiency gains.

What should a startup prove before raising seed funding?

Before raising seed funding, a startup should prove that a specific customer segment has a painful problem, that the product can solve one core workflow, and that users show meaningful behavior such as activation, repeat usage, paid pilots, revenue, referrals, or strong qualitative demand.