The MENA startup ecosystem in 2026 is not slowing down in a simple way. It is becoming more disciplined. Capital is still available, Saudi Arabia is still pulling the region toward larger domestic opportunities, and the UAE remains the fastest regional launchpad. But investors are now rewarding infrastructure, defensibility, regulatory clarity, and credible paths to liquidity more than broad growth narratives.

For founders, the lesson is practical: do not read the region as one market. Treat it as a portfolio of operating choices. Saudi Arabia is where many startups go for scale, government-linked demand, and Vision 2030-aligned sectors. The UAE is where many teams go for speed, licensing flexibility, regional talent, and cross-border capital. The Qatar startup ecosystem offers concentrated access to public programs and enterprise pilots, while the Bahrain startup ecosystem is especially relevant to fintech, regulated products, and a compact GCC launch base. For a Saudi-specific view, start with Hapy’s guide to the startup ecosystem in Saudi Arabia.

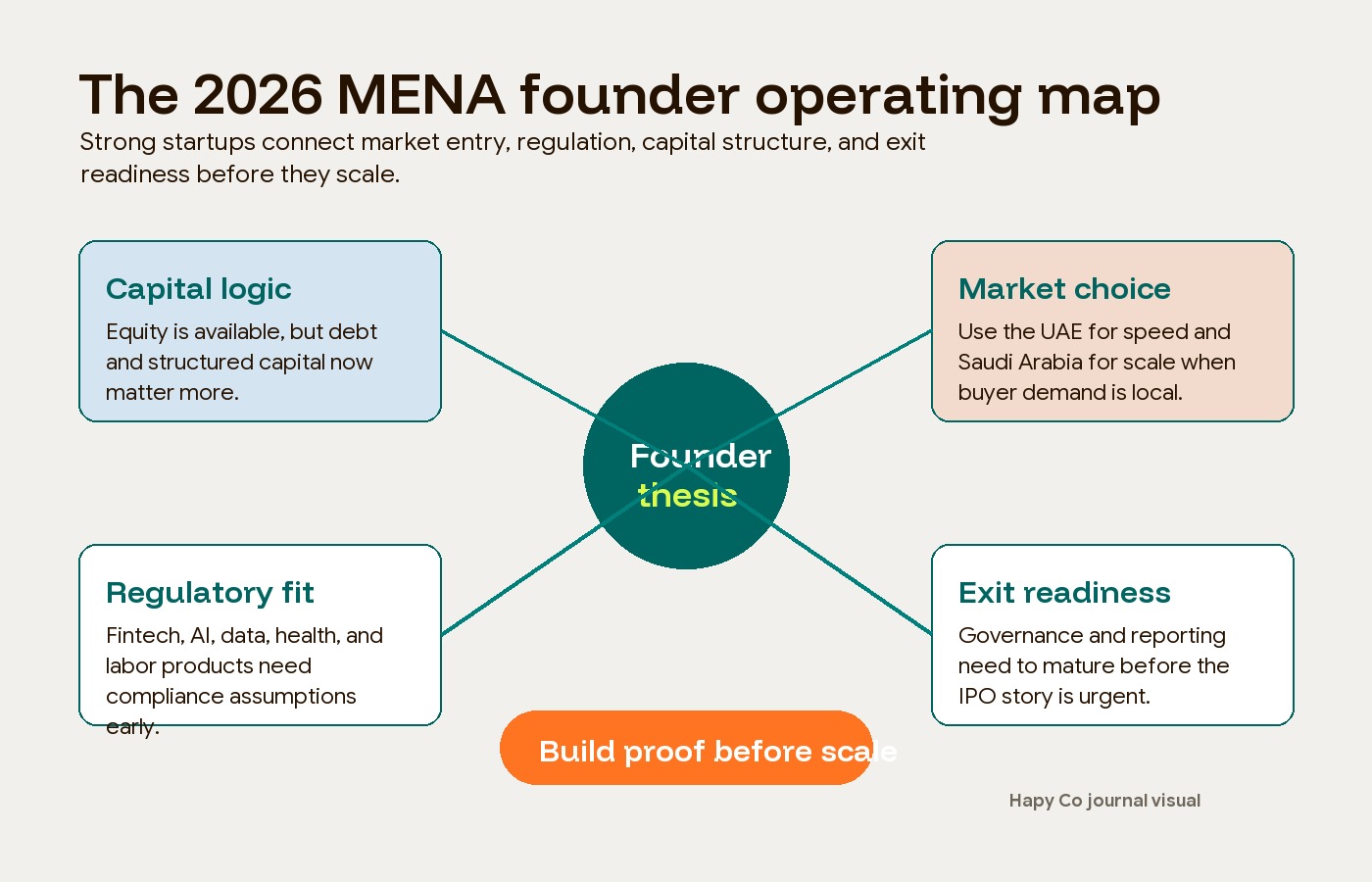

The real opportunity is not just “raise money in MENA.” It is to build a product that fits the new capital logic: revenue-backed, compliance-aware, useful to institutions, and designed for a region where digital infrastructure is becoming national infrastructure.

MENA startup ecosystem 2026: the short version

The short version is this: MENA has matured from an expansion story into a value-realization story. The strongest startups in 2026 are no longer selling investors on market size alone. They are showing why their product belongs inside the region’s next layer of financial infrastructure, AI infrastructure, enterprise software, health systems, logistics, ecommerce operations, or government-backed transformation programs.

That shift is visible in the data. Saudi Arabia reached a historic venture funding total of $1.7 billion in 2025, according to SVC figures reported by Arab News. Semafor, citing MAGNiTT data, also reported that Middle East venture deals hit $3.4 billion in 2025, with Saudi Arabia the largest market at $1.7 billion and the UAE next in line.

Then 2026 started unevenly. Wamda reported that MENA startup funding fell to $941 million in Q1 2026, down 21.5% quarter-on-quarter and 37% year-on-year, as geopolitical tension weighed on dealmaking. March was especially weak: startup funding fell to $48.3 million across 17 startups, an 85% drop from February, according to Wamda.

April showed the market had not disappeared. Wamda reported that MENA startups raised $150 million across 27 deals in April 2026, up 211% month-on-month, but still down 42% year-on-year. The important detail is the structure: half of April’s capital came through debt financing. That tells founders something useful. Investors are still deploying, but they are asking for more protection and clearer revenue logic. That matches the broader startup funding trends in 2026: capital is still available, but weak MVP evidence and vague growth stories are harder to fund.

Why Saudi Arabia is setting the regional operating tempo

Saudi Arabia is now the strongest force shaping the Middle East startup ecosystem because it combines capital, domestic demand, policy direction, and public-market ambition in one place. That does not make it the easiest market. It makes it the market founders cannot ignore if they are building for scale in the GCC.

The Public Investment Fund’s 2026-2030 strategy is a useful lens. PIF says its new strategy moves from rapid growth toward sustained value creation, private-sector participation, and six domestic ecosystems: Tourism, Travel & Entertainment; Urban Development & Livability; Advanced Manufacturing & Innovation; Industrials & Logistics; Clean Energy, Water & Renewables Infrastructure; and NEOM.

For startups, those are not abstract policy labels. They are demand maps. A logistics SaaS company, AI infrastructure provider, industrial automation team, construction-tech platform, tourism operating system, fintech lender, or healthcare workflow product can now position around large domestic buyers rather than only consumer adoption.

Saudi’s broader economy supports the same story. Argaam, summarizing Vision 2030 data, reported that non-oil activities reached 55% of real GDP in 2025 and non-oil government revenue reached SAR 505 billion. Those numbers matter for startups because they show the demand base is not only oil-cycle spending. The economy is deliberately building more non-oil operating capacity, and startups that serve that shift can become suppliers, partners, or acquisition targets.

SVC is one of the clearest examples of how public capital is trying to create private-market depth. Its total committed investments reached $1.2 billion since inception and stimulated $5.9 billion in partner commitments, according to Arab News. The number of VC investors in Saudi Arabia increased from 34 in 2018 to 200 in 2025. That is not just more money; it is more market plumbing.

Funding is active, but the easy narrative is gone

The 2026 startup funding MENA pattern is not “capital winter” or “capital boom.” It is a selective market where funding follows credible operating evidence.

Wamda’s Q1 2026 report shows the split clearly. The UAE led Q1 with $625.8 million across 46 deals. Saudi startups raised $156.7 million across 57 deals. Egypt ranked third with $86 million across 12 deals. Fintech led sector funding with 46% of total investment, followed by proptech and foodtech.

That distribution says two things at once. First, the UAE remains a capital magnet. Second, Saudi Arabia’s deal count shows a broad startup base even when quarterly funding value trails the UAE. For founders, the difference matters. The UAE is often where capital and regional company formation move quickly. Saudi Arabia is where more founders may need patient local execution, local trust, and stronger enterprise sales discipline.

April’s rebound adds another signal. Wamda reported that fintech raised $89.4 million across seven deals in April, while B2B companies captured $95.8 million across 11 deals. This favors companies that sell infrastructure, software, payments, workflow automation, underwriting, compliance, logistics, and enterprise tools. It is less forgiving for consumer startups with high burn and thin differentiation.

The founder takeaway is simple: build the fundraise around risk reduction. Investors want to see market access, regulatory awareness, customer concentration risk, gross margin, collection cycles, and a path to follow-on capital. A good product story still matters, but it has to sit inside a credible operating plan.

The sectors with the strongest 2026 pull

The most attractive sectors in the MENA venture capital story are the ones that solve institutional problems, not just user convenience problems.

Fintech remains the regional anchor because it connects directly to payments, SME credit, embedded finance, open banking, procurement, collections, and financial inclusion. In uncertain markets, financial infrastructure is easier to defend than another lifestyle app.

B2B SaaS and enterprise workflow tools are also stronger than their historical share suggests. As AI lowers the cost of building software, horizontal SaaS will face more competition. But vertical software that owns a regulated workflow, a payment flow, a procurement process, or a compliance burden can still become sticky. For Saudi-specific SaaS context, see Hapy’s guide to the SaaS market in KSA and the broader SaaS technology choices behind those products.

AI infrastructure and applied AI are rising because Saudi Arabia and the UAE are not treating AI as a feature category. They are treating it as national infrastructure. HUMAIN and Saudi Arabia’s National Infrastructure Fund agreed to a financing framework of up to $1.2 billion to develop up to 250 MW of hyperscale AI data center capacity, according to Arab News. For startups, the more immediate opportunity may be less about training frontier models and more about building applied AI products that plug into enterprise, healthcare, finance, legal, education, logistics, and public-sector workflows. That is also the practical angle in our guide to the future of AI in the Middle East.

Healthtech, logistics, ecommerce infrastructure, and foodtech still matter, but the winners will likely be those with a strong operational edge. The 2026 market is rewarding founders who can prove they understand local fulfillment, payment behavior, compliance, procurement, language, trust, and service delivery.

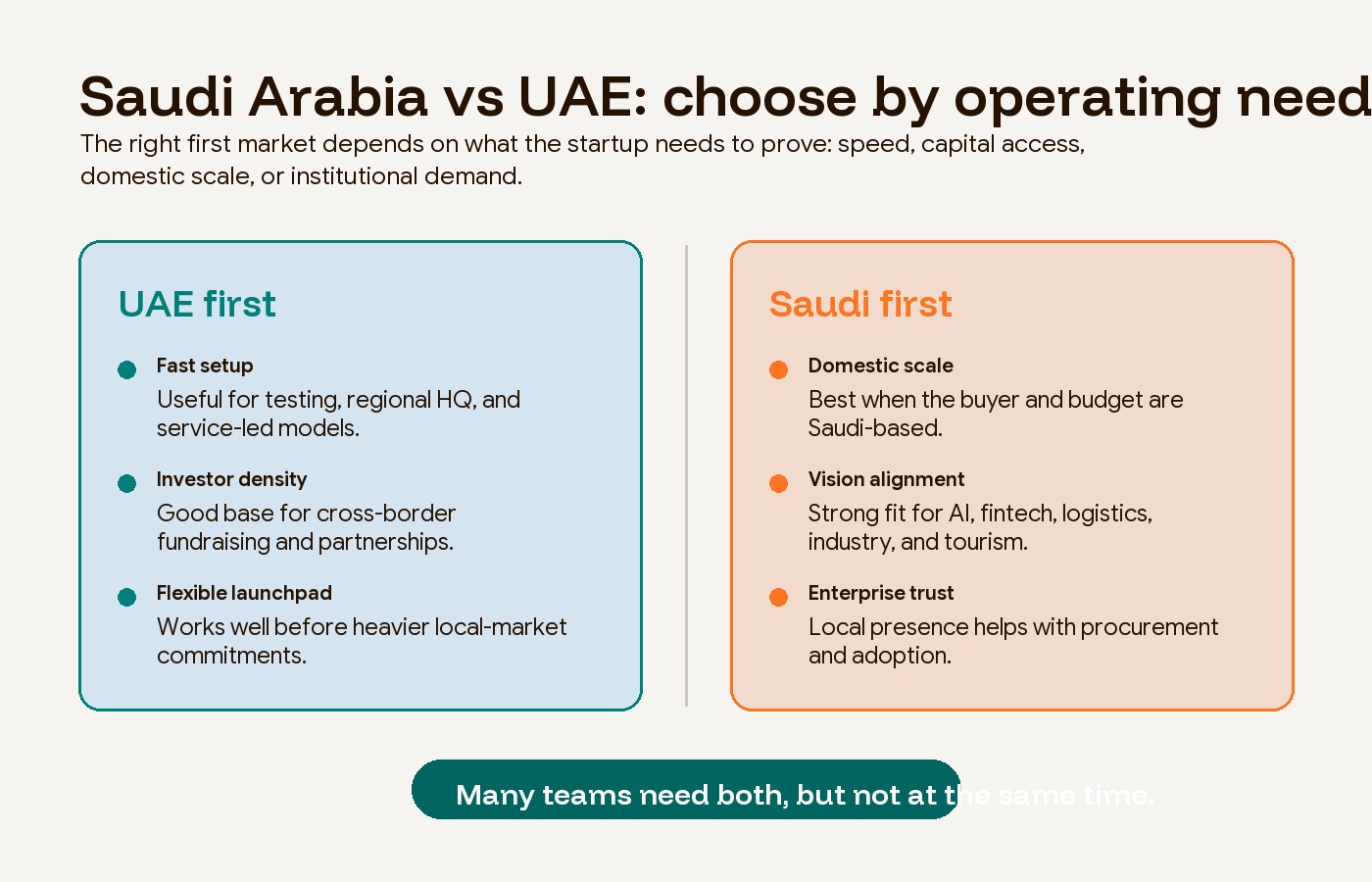

Saudi Arabia vs UAE: choose the market by operating need

Founders often ask whether to start with Saudi Arabia or the UAE. The better question is: what does the startup need first?

If the company needs fast setup, a regional commercial base, global talent access, and a flexible testing environment, the UAE is often the more practical first move. The UAE startup ecosystem guide compares Dubai and Abu Dhabi by commercial speed, institutional access, regulation, and product motion.

If the company needs the largest domestic GCC market, state-aligned demand, Arabic-first enterprise workflows, local procurement relationships, or Vision 2030 sector alignment, Saudi Arabia deserves earlier attention. The upside can be larger, but the sales cycle, compliance work, and relationship-building expectations are usually heavier.

| Founder need | Better first fit | Why it matters |

|---|---|---|

| Fast company setup and regional testing | UAE | Quicker entry, flexible commercial base, strong international founder network |

| Large domestic demand | Saudi Arabia | Bigger local market and deeper alignment with national transformation programs |

| Fintech, AI, logistics, industrial, or government-linked demand | Saudi Arabia | Stronger fit with Vision 2030, PIF ecosystems, and institutional buyers |

| Cross-border services, consulting, media, marketplace, or regional HQ model | UAE | More open regional operating base and mature expatriate business infrastructure |

| Enterprise sales into Saudi buyers | Saudi Arabia | Local presence and trust can matter more than remote selling |

The practical answer may be “both, but in sequence.” Many teams use the UAE for formation, capital access, and regional operations, then build a Saudi go-to-market motion once the product, compliance assumptions, and enterprise narrative are stronger. Others should start in Saudi from day one because the product only makes sense if it is deeply tied to Saudi buyers.

Exit readiness is becoming part of the startup story

The Saudi startup ecosystem is also maturing because founders are starting to think about liquidity earlier. That is healthy, but it creates a new execution burden.

Endeavor Saudi Arabia reported that Saudi exchanges accounted for 106 of 130 GCC IPOs between 2023 and 2025, about 82% of regional listings. It also noted that Nomu expanded from 9 listed companies in 2017 to around 125 by September 2025. In the same report, 23 of 30 high-impact founders surveyed were actively considering going public, while half of those considering IPOs in the next two years said they were not at all or only little prepared for listing requirements.

That gap is one of the most important founder lessons in the region. A public-market story cannot be pasted onto a company at the end. Governance, reporting, leadership depth, risk management, and unit economics need to be built before the IPO conversation becomes urgent.

M&A is also becoming more important. Even during slower months, strategic acquisitions continued across AI, ecommerce, adtech, and services. This matters because not every strong MENA startup will become a public company. Some will become acquisition targets for regional incumbents that need technology, distribution, talent, or category expansion.

What founders should do differently in 2026

The best founder response to the 2026 market is not fear. It is discipline.

First, build for a specific buyer. “MENA is growing” is too vague. A better thesis is: Saudi logistics companies need compliance-aware fleet finance tools; UAE-based B2B marketplaces need embedded working-capital products; GCC healthcare operators need AI-supported intake and patient workflow systems; tourism operators need multilingual booking and operations software before peak-event demand.

Second, design the MVP around proof, not feature volume. In a selective funding market, an MVP should prove demand, pricing, implementation complexity, and buyer urgency. That is especially true for founders selling into Saudi Arabia, where enterprise trust and local execution matter. Hapy’s work around MVP development in KSA is built around this exact problem: founders need something credible enough to sell, learn, and raise against without overbuilding too early.

Third, make compliance part of product strategy. Fintech, healthtech, AI, data, ecommerce, and workforce platforms all face regulatory questions. Do not leave those questions as investor diligence surprises. Turn them into a visible part of the roadmap, especially if the team is working with Arab clients in the Middle East and needs local trust from the start.

Fourth, prepare for flexible capital. The April 2026 debt-heavy rebound shows that some startups will need to think beyond straight equity. Venture debt, revenue-based financing, strategic capital, and government-linked programs may all matter depending on the model. Founders should understand which instruments match their margins, cash cycles, and collateral.

Fifth, treat hiring as an operating system. The report behind this article flagged a tighter 2026 recruiting environment, including candidate quality, process speed, compensation transparency, and retention. That lines up with what many startup teams feel on the ground: the bottleneck is not always sourcing. It is deciding who the company needs, moving fast, and designing roles around outcomes rather than vague credentials.

A founder checklist for the MENA startup ecosystem

Use this checklist before committing to a market-entry plan or fundraising story:

- Define the first country by operating need, not ego.

- Name the exact buyer and the budget line your product fits.

- Identify whether the product is exposed to fintech, data, AI, health, labor, tax, or sector-specific regulation.

- Build a 90-day MVP plan that proves demand and pricing before adding secondary features.

- Decide whether the company needs Saudi local presence, UAE regional operations, or both.

- Show how the model performs under slower collections, longer enterprise sales cycles, and smaller cheque sizes.

- Prepare a capital plan that includes equity and non-equity options.

- Build reporting habits early if an IPO, strategic acquisition, or larger institutional round is a realistic future path.

The broader point is that founders should stop treating MENA as a hype cycle. The region is becoming a serious operating environment. That is good news for teams with product judgment, local context, and enough discipline to earn trust before chasing scale.

Conclusion: the next MENA winners will look more operational

The MENA startup ecosystem in 2026 is still full of opportunity, but the shape of opportunity has changed. Saudi Arabia is setting the scale agenda through Vision 2030, PIF ecosystems, SVC-backed market depth, AI infrastructure, and public-market ambition. The UAE remains the region’s most efficient launchpad for capital, company formation, and cross-border growth. Fintech, B2B software, AI infrastructure, healthtech, logistics, and ecommerce infrastructure are still attracting attention because they solve real operating problems.

The founders most likely to win are the ones who read those signals correctly. They will not just build “for MENA.” They will build for a specific buyer, in a specific regulatory context, with a product that can survive selective capital and still grow into the region’s institutional demand.

For teams planning a Saudi or GCC product launch, the next step is not a bigger pitch deck. It is a tighter operating thesis, a focused MVP, and a market-entry plan that proves why the product belongs in the region now.