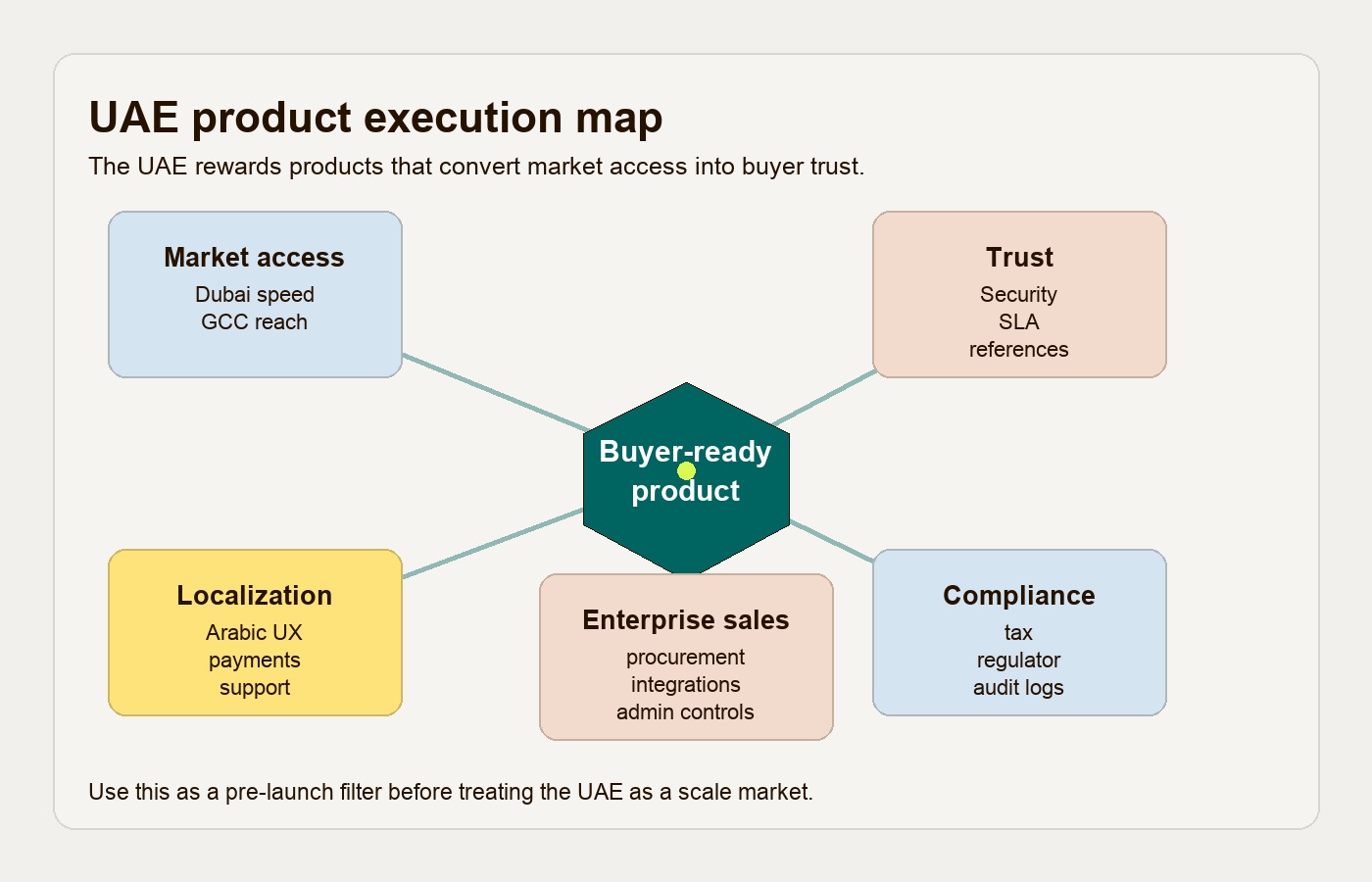

The UAE startup ecosystem is no longer just a fundraising destination. It is a product-launch market where founders are judged by how well they localize, sell to serious buyers, handle regulation, and turn a promising MVP into a trusted operating system.

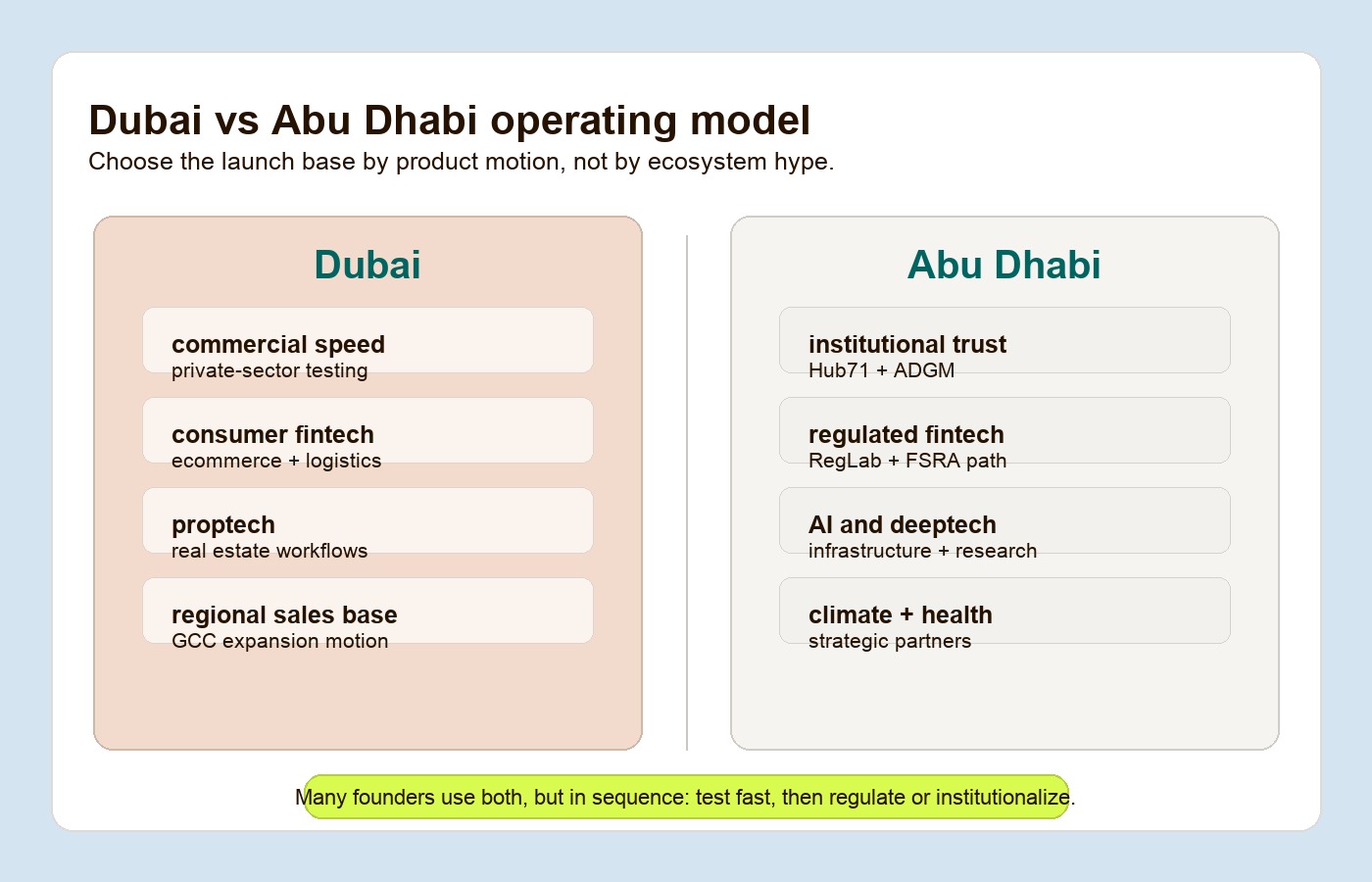

That is the useful 2026 read. Dubai gives founders speed, commercial density, private capital, regional headquarters energy, and a strong Dubai digital economy agenda. Abu Dhabi gives founders sovereign-backed infrastructure, Hub71, ADGM, research depth, and more patient institutional pathways. Both matter, but they are not interchangeable.

For GCC founders, international founders, and innovation teams, the question is not “Is the UAE good for startups?” It is. The better question is: which UAE operating environment matches the product you are building, the buyer you need, and the compliance burden you cannot avoid?

UAE startup ecosystem in 2026: the useful read

The UAE is attractive because it combines four things founders usually have to assemble separately: company formation options, regional capital access, English-speaking business infrastructure, and proximity to GCC buyers. That combination makes it a strong base for fintech, AI, logistics, ecommerce infrastructure, healthtech, climate, proptech, and enterprise software.

The capital signal is still active, but it is more selective. Wamda reported that MENA startups raised $326.6 million across 62 deals in February 2026, with the UAE leading the region at $162.8 million across 23 startups. In March, the market paused sharply: Wamda reported $48.3 million across 17 deals, with the UAE still leading at $36.8 million across eight deals.

That pattern matters more than the monthly headline. Capital has not disappeared, but it is clustering around founders who can show business demand, regulatory awareness, implementation depth, and believable unit economics. This is especially true for UAE fintech startups, UAE AI startups, and B2B platforms selling into banks, real estate groups, logistics operators, healthcare networks, and government-linked buyers.

The practical founder takeaway is simple: treat the UAE as a serious launch market, not a presentation backdrop. A thin product can get meetings. It will not keep them.

Dubai startup ecosystem: speed, commerce, and market testing

The Dubai startup ecosystem is strongest when the company needs fast commercial learning. Dubai has the density of investors, founders, free zones, service providers, events, private wealth, and regional operators that make it easier to test a product narrative quickly.

The public strategy supports that pace. The Dubai Economic Agenda D33 targets AED 32 trillion in total economic goals over 10 years, including AED 100 billion in annual economic contribution from digital transformation, a program to support 30 companies in new sectors to become global unicorns, and Sandbox Dubai for testing and marketing new products and technologies.

That does not mean every startup should choose Dubai by default. Dubai is useful when the product benefits from speed, private-sector demand, regional sales, and quick market feedback. It is less forgiving when the founder still has a vague buyer, weak onboarding, unclear compliance assumptions, or a product that only works when the founder is in the room.

Dubai is especially relevant for:

- Commercial SaaS that helps companies manage operations, finance, HR, sales, procurement, or customer service.

- Consumer and SME fintech products that need retail distribution, payments partnerships, or regional brand trust.

- Proptech and real estate workflow tools connected to leasing, valuation, property management, facilities, mortgages, or tokenization.

- Logistics, ecommerce, and marketplace infrastructure that benefits from Dubai’s trade and regional hub position.

- AI products that help enterprises automate narrow workflows without creating governance risk.

The product bar is trust. Dubai buyers move quickly, but they still expect the basics: clean bilingual communication when needed, fast support, payment reliability, enterprise security, clear pricing, and a product that understands local procurement and decision-making.

Abu Dhabi startups: infrastructure, capital, and deeptech patience

Abu Dhabi is built differently. Its startup system is more institutional, more research-led, and more connected to sovereign-backed sectors. That makes it a better fit for founders building around fintech infrastructure, regulated digital assets, AI infrastructure, climate, advanced health, defense-adjacent technology, and enterprise products that need large strategic partners.

Startup Genome’s Abu Dhabi profile places the city in the #41-50 global emerging ecosystem range, with $73 billion in ecosystem value for H2 2023 through 2025 and $4.8 billion in total VC funding from 2021 through 2025. The same profile highlights Hub71 as the central startup platform, with Abu Dhabi strength in AI-native startups, R&D, fintech, climatetech, and Web3/digital assets.

Hub71 matters because it is not only a coworking brand. It is a market-access layer. Startup Genome describes Hub71 as Abu Dhabi’s global tech ecosystem, backed by the Government of Abu Dhabi and Mubadala Investment Company, with access to capital, markets, partners, incentives, and talent. For a founder, that is useful when the product needs more than early users. It needs institutional credibility.

ADGM adds the financial-regulatory layer. ADGM says its FSRA was the first in the region to launch the ADGM RegLab regulatory sandbox, giving fintechs a controlled environment to test innovation under regulator guidance. That is useful for institutional fintech, digital assets, custody, tokenization, compliance infrastructure, and products that need regulator-facing maturity before they scale.

Abu Dhabi is less useful for founders who simply want a fast, low-friction MVP test. It is more useful when the product needs sovereign-grade infrastructure, sector partnerships, research depth, or a credible route into conservative enterprise buyers.

Dubai vs Abu Dhabi: choose by product motion

Dubai and Abu Dhabi are complementary, but founders should not blur them into one generic UAE strategy.

| Founder need | Better first fit | Why it matters |

|---|---|---|

| Fast commercial testing | Dubai | More private-sector density, regional HQ activity, events, agencies, and founder-service infrastructure |

| Institutional fintech or digital assets | Abu Dhabi | ADGM, FSRA, RegLab, and deeper fit for regulated financial services infrastructure |

| Consumer fintech, ecommerce, or logistics | Dubai | Faster access to merchants, operators, consumer demand, and cross-border commercial networks |

| AI infrastructure or research-heavy AI | Abu Dhabi | Stronger link to sovereign infrastructure, advanced computing, Hub71+ AI, and research partnerships |

| Proptech and real estate commercialization | Dubai | Larger visible real estate market, private wealth, brokerage networks, and investor demand |

| Climate, energy, and industrial decarbonization | Abu Dhabi | Masdar, TAQA, ADNOC adjacency, climate programs, and infrastructure-led buyer pathways |

| Government pilots and regulatory modernization | Both | Dubai is strong for sandbox and service innovation; Abu Dhabi is strong for regulated and institutional pathways |

| Regional sales base for GCC expansion | Dubai | Easier commercial travel, international founder base, and sales-led operating culture |

The sequencing can also be mixed. A founder may incorporate or test commercial demand in Dubai, then build a regulated Abu Dhabi path once the product needs ADGM, Hub71, or a sector-specific institutional partner. Another founder may start in Abu Dhabi because the product only makes sense near the regulator, hospital network, AI infrastructure partner, or sovereign-backed buyer.

Accelerators and ecosystem programs: fit list

Founders should choose UAE accelerators by the product risk they need to reduce, not by brand recognition alone.

| Program or ecosystem | Best fit | Product risk it helps reduce |

|---|---|---|

| Hub71 | AI, fintech, climate, healthtech, digital assets, enterprise software | Market access, investor credibility, partner introductions, Abu Dhabi landing support |

| DIFC Innovation Hub | Fintech, insurtech, regtech, wealthtech, embedded finance | Financial-services ecosystem access, banking conversations, investor visibility |

| DFSA Innovation Testing Licence | Regulated fintech products in or from DIFC | Controlled live testing, licence restrictions, regulator engagement, transition to authorisation |

| ADGM RegLab | Institutional fintech, digital assets, tokenization, compliance tooling | Controlled testing under FSRA guidance before full financial-services permission |

| Dubai Future District Fund | Future-economy startups and VC funds tied to Dubai’s innovation thesis | Capital access, fund network, Dubai Future District positioning |

| Sandbox Dubai | Emerging technologies that need policy or regulatory testing | Public-sector testing, rule modernization, controlled pilots |

| Oraseya Capital and SANDBOX | Pre-seed and seed tech startups in Dubai | Early capital, structured acceleration, Dubai Silicon Oasis ecosystem access |

| Dubai Future Accelerators | Startups solving government or strategic city challenges | Problem-led pilots, public-sector buyer discovery, implementation proof |

The hidden question is implementation capacity. A program can open doors, but it cannot replace the work of building a secure product, preparing pilot metrics, documenting compliance assumptions, training local users, and selling beyond the first warm introduction.

Sector opportunity matrix for UAE founders

The strongest UAE startup opportunities sit where capital, government strategy, local buyer pain, and product execution overlap.

| Sector | UAE opportunity | What founders should build first | Main execution risk |

|---|---|---|---|

| Fintech | Payments, SME credit, open finance, digital assets, Islamic finance, compliance | Trust layer: onboarding, KYC, reconciliation, audit logs, fraud controls, partner APIs | Treating regulation as a later legal task |

| AI | Government services, enterprise copilots, workflow automation, Arabic AI, AI governance | Narrow workflow product with permissions, human review, evaluation, and reporting | Building a demo that cannot survive enterprise use |

| Climate | Carbon accounting, green procurement, energy optimization, real estate efficiency, water systems | Data model, verification workflow, buyer ROI, reporting outputs, integrations | Selling sustainability claims without operational proof |

| Proptech | Leasing, valuation, property management, smart buildings, tokenized assets, mortgage workflows | Workflow software for brokers, landlords, tenants, lenders, and facility teams | Mistaking real estate demand for automatic product adoption |

| Healthtech | Telehealth, chronic-care workflows, diagnostics, hospital operations, precision medicine | Privacy-first workflow with clinical handoff, Arabic support, and clear accountability | Underestimating clinical governance and data standards |

| Logistics and ecommerce | Fulfillment, payments, last-mile operations, inventory, customs, B2B commerce | Operating dashboard, exception handling, payment flow, integrations, service SLAs | Building marketplace surface without operational depth |

| Enterprise SaaS | Finance ops, procurement, HR, customer support, sales ops, compliance | Security, admin controls, role permissions, bilingual UX where needed, onboarding | Weak enterprise readiness and unclear budget owner |

The UAE is a strong test market for products that need both local adaptation and regional ambition. It is a weak market for generic SaaS positioning. Buyers have seen enough tools. They want products that understand the workflow, the language, the compliance boundary, and the service expectation.

Compliance is product scope, not paperwork

The UAE rewards founders who build trust into the product early. That trust can come from regulatory fit, clear data handling, auditability, enterprise security, or simply making the product feel native to the buyer’s operating environment.

For fintech, the choice of regulatory home matters. A retail-facing payment or virtual-asset product may need a different path from an institutional custody, tokenization, or compliance platform. The DFSA explains that the Innovation Testing Licence is a licensed sandbox where eligible firms can test for a specific period, typically 12 months, under restrictions before applying to exit the ITL or withdraw. ADGM’s RegLab is similarly relevant for fintechs ready to test innovative solutions in a controlled environment.

For tax and entity design, founders should not assume a free zone means no compliance. UAE corporate tax, free-zone qualifying income rules, substance expectations, audits, and transfer-pricing documentation can become product-company issues when customers, investors, or acquirers diligence the business. Early-stage teams should get professional advice before relying on a 0% free-zone assumption or deferring tax readiness until a round is underway.

For AI, the compliance layer is also a product layer. If a UAE AI startup sells to government, finance, health, legal, HR, education, or critical infrastructure, buyers will ask what the model used, who approved the output, how errors are corrected, whether data leaves the environment, and what logs exist. Hapy’s guide to the future of AI in the Middle East is useful context for why regional AI ambition is moving from experimentation into infrastructure.

For Arabic and localization, the product question is not only translation. It is trust. Arabic UX, right-to-left patterns, names, addresses, payment methods, local support expectations, and culturally familiar onboarding can affect conversion more than another feature. Hapy’s guide to Arabic website design basics is relevant when the product or marketing site needs to earn trust from Arabic-speaking users.

Founder challenges in the UAE

The first challenge is false speed. The UAE can make setup, meetings, and introductions feel fast. Product adoption is slower. Real buyers still need budget, stakeholder alignment, security review, procurement, integration, training, and proof that the product will not create operational risk.

The second challenge is overgeneralizing the GCC. A product that works in Dubai may still need different pricing, Arabic depth, support hours, legal terms, and sales motion for Abu Dhabi, Riyadh, Doha, Kuwait City, or Manama. The UAE can be a launch base, but it is not the whole GCC.

The third challenge is regulated ambition. Fintech, AI, healthtech, proptech, and climate products all touch rules, data, or institutional risk. The founder who treats compliance as a late-stage cost will lose time later. The better founder turns compliance into product advantage: clearer logs, safer permissions, better admin controls, better reporting, better customer confidence.

The fourth challenge is enterprise sales readiness. The UAE has sophisticated buyers. They will ask for references, security documentation, commercial terms, support expectations, SLAs, implementation steps, and local accountability. A founder-led demo is not the same as a deployable enterprise product.

The fifth challenge is talent and operating cost. The UAE can attract global talent, but senior talent, office requirements, visas, sales hiring, legal support, and customer success can raise burn quickly. Founders should model the cost of learning in-market, not only the cost of incorporation.

What founders should build before they raise or launch

Founders entering the UAE should build the smallest serious product, not the smallest possible demo.

For fintech, that means onboarding, KYC assumptions, reconciliation, audit trails, fraud controls, payment reliability, permissions, and a clear regulator or partner path. Do not pitch a finance product if the product cannot explain how money, identity, and risk move through the system.

For AI, build a workflow-specific product with measurable before-and-after value. The product should show sources, confidence, human review, escalation, logs, and admin controls. “AI assistant” is not enough. UAE buyers need to know what the system does when it is wrong.

For climate and proptech, build around asset owners and operators. Carbon reporting, building efficiency, smart maintenance, tenant workflows, green procurement, and energy optimization only work when the product connects to real operational data and decision cycles.

For healthtech, start with the care workflow. A patient-facing app is rarely enough. Teams need clinical accountability, privacy, Arabic support where relevant, hospital integration assumptions, and a clear view of who owns the outcome.

For enterprise SaaS, define the budget owner before building more features. The UAE has many digitally mature companies, but “digital transformation” is not a buyer. Finance, operations, procurement, HR, legal, customer service, or IT needs to own a problem the product solves.

For international founders, Hapy’s guide to the MENA startup ecosystem in 2026 is a useful companion because the UAE often works best as a regional base, not a market in isolation. Founders planning a Saudi expansion should also compare the UAE path with MVP development in KSA, where enterprise trust and localization usually require a heavier local motion.

UAE product-readiness checklist

Use this checklist before committing to a UAE launch, accelerator application, or fundraising story.

| Readiness area | Minimum standard before scaling |

|---|---|

| Buyer | One named buyer role, one urgent workflow, and a clear budget owner |

| Market choice | Dubai, Abu Dhabi, or both chosen for operating fit, not status |

| Product wedge | A specific job-to-be-done, not a broad fintech, AI, climate, or proptech claim |

| Localization | Arabic and English needs, payment behavior, addresses, support, and cultural trust reviewed |

| Compliance | Regulatory exposure mapped for fintech, AI, health, data, tax, labor, or sector rules |

| Security | Admin controls, role permissions, logs, data handling, and incident response basics ready |

| Pilot design | Success metric, timeline, implementation owner, and post-pilot decision rule documented |

| Integrations | Banking, ERP, CRM, identity, property, logistics, health, or government-system needs identified |

| Pricing | Pilot price, enterprise path, and renewal logic matched to buyer value |

| Expansion | Clear view of what changes for Saudi Arabia, Qatar, Bahrain, Oman, or wider MENA |

If several rows are vague, slow down. The UAE rewards speed only when the product is ready to use that speed.

The founder takeaway

The UAE startup ecosystem is strongest for founders who can combine regional ambition with product execution. Dubai gives speed, commercial density, private capital, and a strong launch environment. Abu Dhabi gives infrastructure, Hub71, ADGM, research depth, sovereign-backed sectors, and a stronger path for regulated or deeptech products.

The harder truth is that UAE buyers and investors are becoming more selective. They are not looking for generic expansion stories. They are looking for products that can localize, integrate, prove value, and handle trust.

Build for the meeting after the first meeting. Build the compliance layer before it becomes a blocker. Build the Arabic and enterprise experience before trust leaks. Build a product that can earn a pilot, survive implementation, and expand across the GCC with evidence behind it.

That is the real opportunity in the UAE startup ecosystem: not just raising in the region, but launching products that are ready for the region’s operating reality.