The Bahrain startup ecosystem is useful for founders who are building products where trust matters early: fintech, B2B SaaS, compliance software, Islamic finance, cybersecurity, AI for financial services, SME finance, and regulated digital infrastructure.

That is the practical read for 2026. Bahrain is not the largest GCC market, and it should not be treated as a shortcut around regulation. Its advantage is different: a compact operating base, a financial-services history, a single central-bank supervisor for many fintech categories, visible ecosystem builders, local cloud infrastructure, and public programs that can reduce some talent and market-entry friction.

The founder mistake is to read those signals as permission to build a light demo. In Bahrain, the best opportunities sit close to banks, regulators, enterprise buyers, government-linked programs, and financial infrastructure. That means the MVP needs more than a clickable prototype. It needs the first version of identity, permissions, audit trails, data handling, customer support, security, and compliance logic.

For GCC founders and fintech founders, Bahrain works best when it is used as a disciplined launchpad: small enough to learn, serious enough to expose product risk, and connected enough to support a wider GCC expansion story.

Bahrain startup ecosystem in 2026: the useful read

Bahrain’s startup story is strongest when it is read through product fit, not ecosystem promotion. The country has been positioning itself around financial services, fintech, ICT, cybersecurity, AI, and regional business access. Bahrain EDB describes the economy as one of the GCC’s most diversified, with strengths in financial services, ICT, manufacturing, logistics, and tourism, plus 100% foreign ownership in most non-oil sectors.

The 2026 visibility signal is real. Zawya, citing Startup Genome’s Global Startup Ecosystem Report 2026, reported that Bahrain’s tech startup ecosystem reached US$1.6bn in ecosystem value, up 759% over five years, and ranked among the top five MENA ecosystems for performance. The same report highlighted fintech, blockchain, AI, and digital innovation as core engines.

Those numbers matter, but they do not remove execution risk. A founder entering Bahrain still needs to answer four questions:

- Does the product need Bahrain’s regulatory, banking, or enterprise context?

- Can the first version satisfy trust requirements without becoming overbuilt?

- Which program reduces the biggest risk: market access, licensing, capital, talent, or product capability?

- What proof from Bahrain would make expansion into Saudi Arabia, UAE, Qatar, Kuwait, or Oman more credible?

If the answer is only “Bahrain is cheaper,” the thesis is weak. If the answer is “Bahrain gives us a controlled place to build a compliant product for financial or enterprise buyers,” the market starts to make sense.

Fintech regulation is the center of gravity

Bahrain’s fintech advantage starts with regulatory clarity. The Central Bank of Bahrain is the main supervisor for financial services, and its FinTech & Innovation Unit oversees sandbox participation, testing progress, and collaboration across the fintech ecosystem. The CBB says its regulatory sandbox lets startups, fintech firms, and licensees test innovative banking and financial solutions in a controlled environment before scaling.

That matters because a regulated fintech MVP is not only a product experiment. It is also a risk experiment. The CBB’s Regulatory Sandbox Framework is open to CBB licensees and local or foreign companies intending to test innovative financial services. It requires applicants to show innovation, customer benefit, major risk identification, CDD and AML/CFT compliance, and customer confidentiality.

The operational details are important for founders:

- The application fee is BD 100.

- The CBB states that it will provide a formal decision within 15 calendar days after all required documentation is submitted in acceptable form.

- The sandbox duration is up to 12 months from authorization.

- Participants must open a client money account with a CBB-licensed retail bank when handling volunteer customer funds.

- Participants must maintain CDD, AML/CFT, confidentiality, onboarding, customer communication, risk disclosure, complaints, and reporting processes during testing.

This changes MVP scope. A fintech founder cannot safely leave identity, money movement, customer disclosure, records, complaint handling, and risk controls until “after validation.” Those are part of validation.

For a deeper product view of money movement, onboarding, and regulated banking features, Hapy’s guide on how to create a banking app is a useful companion.

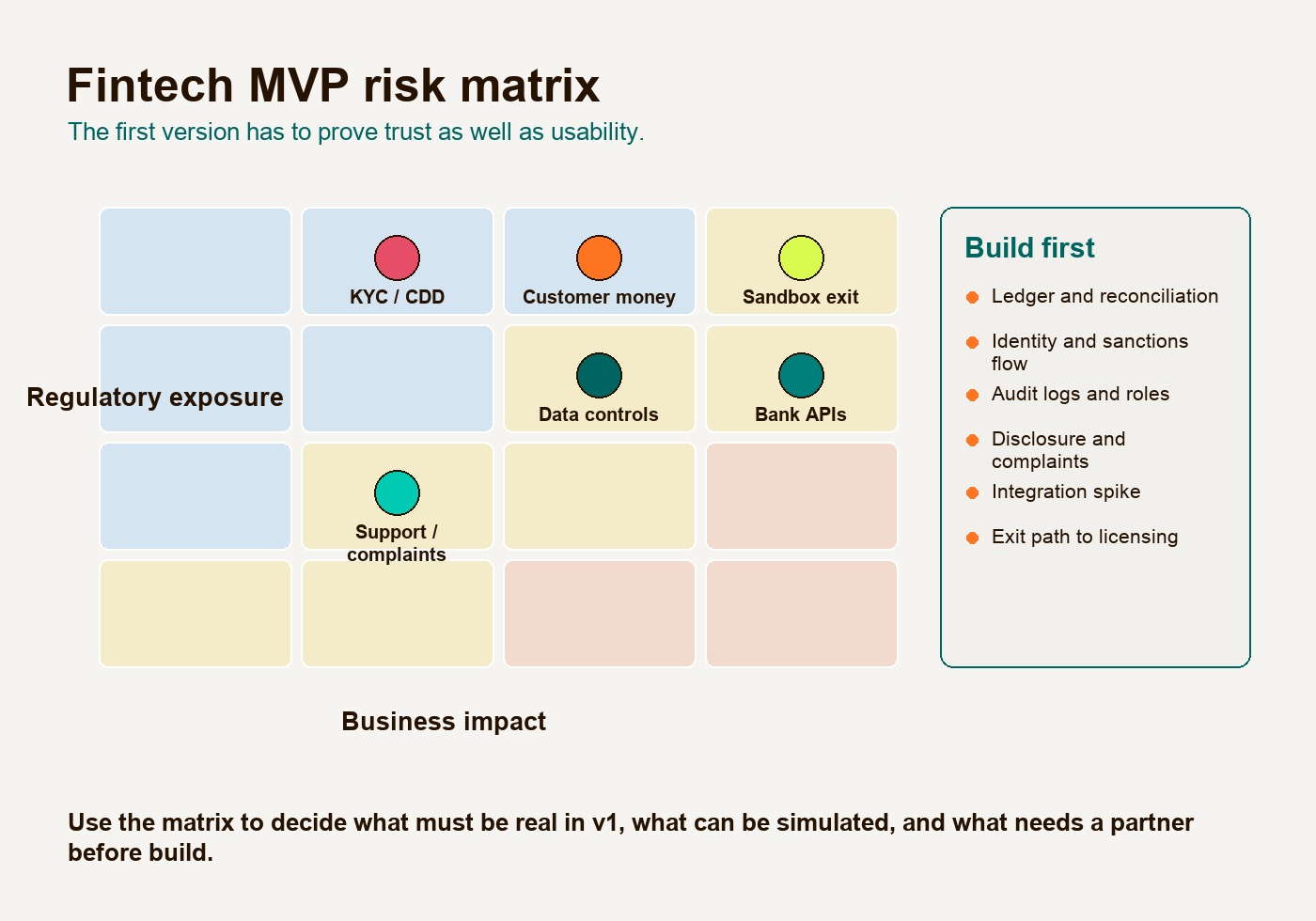

The fintech MVP risk matrix

The Bahrain fintech MVP should be scoped around risk before features. Founders should decide which risks must be solved in version one, which can be simulated, and which require a partner, legal opinion, or sandbox discussion before build.

| MVP risk | Why it matters in Bahrain | Build implication |

|---|---|---|

| Licensing path | The CBB may relax some requirements case by case, but core AML/CFT and confidentiality requirements remain | Map the regulated activity before finalizing the product flow |

| Customer money | Sandbox participants handling volunteer funds need a client money account with a CBB-licensed retail bank | Design ledger, reconciliation, and bank-account workflows early |

| KYC and CDD | Identity checks and customer due diligence are not optional in financial testing | Build onboarding as a compliance workflow, not just a sign-up screen |

| Data protection | Personal and financial data requires controlled access, storage, and transfer assumptions | Include consent, retention, audit logs, and access controls in the MVP |

| Security | Financial buyers will ask about incident handling, access, monitoring, and infrastructure | Use role permissions, event logs, secure environments, and documented response steps |

| Partner APIs | Banking, open banking, payment, and compliance vendors can drive timeline risk | Spike the riskiest integration before promising pilot dates |

| Customer support | Volunteer users still need disclosure, complaints, and issue-handling channels | Add support workflows before live testing |

| Sandbox exit | A test that cannot graduate into licensing creates rework | Build the MVP with a credible route to post-sandbox operations |

The practical rule: build the smallest serious product, not the smallest possible demo. If the product touches money, identity, credit, deposits, investments, digital assets, or banking data, the MVP should prove trust as much as usability.

Bahrain SaaS opportunities are enterprise-led

Bahrain SaaS opportunities are less about consumer scale and more about specialist enterprise demand. The strongest areas sit near financial services, cybersecurity, SME finance, Islamic finance, operations, healthcare workflows, education, logistics, procurement, HR, and compliance.

Cloud infrastructure helps. AWS says its Middle East presence includes the AWS Middle East (Bahrain) Region, giving regional customers more choice for cloud workloads. For SaaS founders selling to financial or public-sector-adjacent buyers, local or regional cloud availability can support latency, resilience, and data-location conversations. It does not solve compliance on its own, but it removes one common blocker.

The product bar is enterprise readiness:

- Admin controls and role-based access.

- Bilingual or Arabic-aware UX where the buyer needs it.

- Audit logs and exportable reports.

- Clear data ownership and retention.

- Integration assumptions for bank, ERP, CRM, identity, payment, or government systems.

- Implementation support that works after the founder leaves the room.

For B2B SaaS and custom workflow products, Bahrain can be a good place to prove a focused system before selling across the GCC. Hapy’s custom software development services buyer guide is relevant when the question becomes whether to build a narrow MVP, a custom internal system, or a larger platform.

Program comparison for Bahrain founders

Bahrain’s support environment is useful because different institutions reduce different risks. Founders should not apply everywhere. They should pick the program that matches the current bottleneck.

| Program or institution | Best fit | What it helps reduce | Founder caution |

|---|---|---|---|

| Bahrain EDB | International founders, scaleups, regional HQs, sector investors | Market-entry information, setup guidance, sector context, investor-facing credibility | It helps you enter; it does not validate the product for you |

| CBB Regulatory Sandbox | Fintech, payments, open banking, digital assets, regtech, financial infrastructure | Controlled testing path, regulator engagement, defined sandbox obligations | Core AML/CFT, confidentiality, customer-money, and risk obligations still matter |

| Bahrain FinTech Bay | Fintech founders, bank-facing startups, ecosystem partnerships | Programs, incubation, financial-institution access, investor and ecosystem connections | Program access is useful only if the product has a clear banking or fintech use case |

| NBB Innovation Programme | Early fintech talent and AI-driven banking ideas | Mentorship, banking context, demo-day exposure, potential banking conversations | A bank challenge is not the same as a production contract |

| Tamkeen | Bahrain-based hiring, training, digitization, and enterprise support | Talent cost, upskilling, wage support, digital enablement, business support | Program terms change; check current eligibility before building the financial model |

| Al Waha Fund of Funds | VC ecosystem, regional funds, venture-backed growth | Fund-manager presence and capital-network depth | It is fund-of-funds infrastructure, not a direct grant for every startup |

| Spring Studios and venture studios | Fintech or venture concepts needing hands-on build capability | Product, engineering, design, legal/regulatory, fundraising, and operating support | Studio economics and control need careful founder alignment |

This comparison is where Bahrain becomes more practical than it first looks. A fintech founder may need CBB first, Bahrain FinTech Bay second, and a venture studio only if the team lacks product or regulatory execution capacity. A SaaS founder may need EDB and Tamkeen more than a fintech program. A cross-border fintech infrastructure startup may need all of them, but in sequence.

Bahrain FinTech Bay describes itself as the kingdom’s leading fintech hub, with strategic focus areas including stablecoins, digital assets, tokenization, microfinancing, SME lending, and AI. NBB’s 2025 Innovation Programme, run with Bahrain FinTech Bay, gave the winning team US$10,000 and a three-month incubation period, which shows the kind of bank-linked experimentation available to early teams.

Spring Studios is a different model. It says it is backed by Bahrain’s Al Waha Fund of Funds and Salica Investments, and offers founders in-house capability across product, engineering, UX/UI, sales, marketing, licensing, and more. That can help when the hardest risk is not only capital, but building a product that can clear the first serious buyer or regulator conversation.

Cost and talent advantages are real, but they are not the strategy

Bahrain can be cost-competitive. An EDB/KPMG financial-services cost report found Bahrain’s annual operating cost for a representative financial-services business was 11% below the GCC average and up to 27% lower than peer jurisdictions. The same report also found Bahrain’s annual cost of living was 23% below the regional average in the selected GCC comparison.

That matters for runway. Lower operating cost can buy time for regulated product discovery, partner integrations, hiring, and market entry. But cost is not a substitute for buyer demand.

Founders should use cost advantage in three practical ways:

- Fund compliance work earlier, not later.

- Hire or train local operators who understand Bahrain and GCC buyer expectations.

- Spend more time with banks, enterprises, and program operators before expanding scope.

Tamkeen should be treated the same way. Its value is not that it makes the business “subsidized.” Its value is that it may reduce specific talent, training, wage, or digitization constraints when eligibility fits. Founders should check the current Tamkeen support-program catalogue before assuming a program will cover a role, software purchase, or salary plan.

Founder challenges in Bahrain

The first challenge is regulated product weight. Bahrain can make the regulatory path clearer, but clarity does not make the product lighter. A fintech MVP needs stronger foundations than a normal SaaS MVP.

The second challenge is market size. Bahrain is useful as a testbed and GCC base, but most startups need a Bahrain-plus-GCC thesis. The question is not only “Can we sell in Bahrain?” It is “What will Bahrain help us prove before Saudi, UAE, Qatar, Kuwait, or Oman?”

The third challenge is enterprise trust. Financial institutions, government-linked entities, and large companies will care about data handling, security, support, procurement, Arabic communication where relevant, and implementation ownership. A fast demo can create interest. It rarely creates adoption.

The fourth challenge is local operating reality. Company setup, banking relationships, physical presence, sector licensing, contracts, and hiring all take management attention. Founders should build timeline buffers instead of treating incorporation as a side task.

The fifth challenge is cultural and buyer context. GCC sales depends on trust, responsiveness, clarity, and relationship quality. Hapy’s guide to working with Arab clients in the Middle East is useful when a founder needs to understand how communication and decision-making affect product adoption.

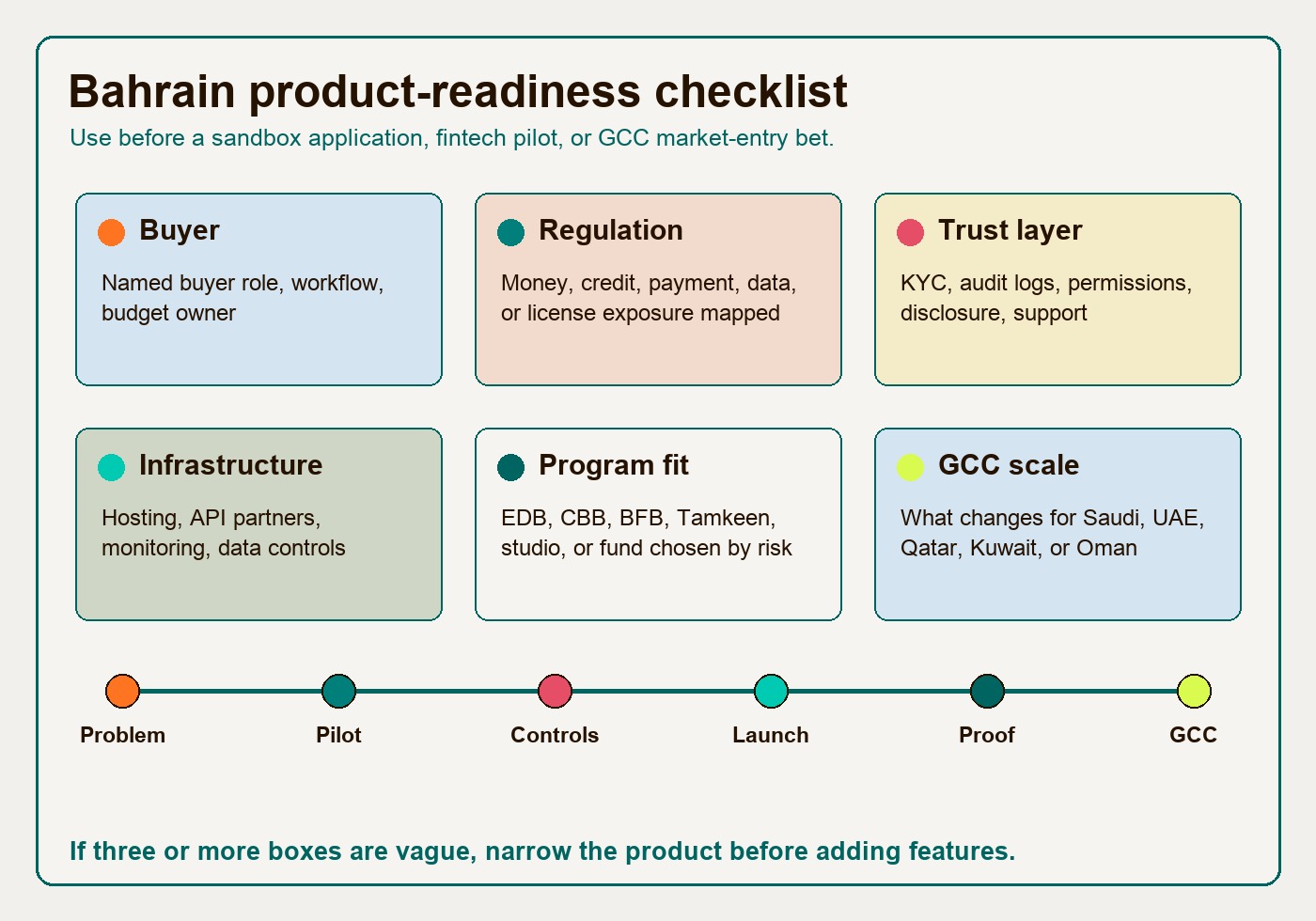

Bahrain product-readiness checklist

Use this checklist before committing to a Bahrain launch, sandbox application, fintech pilot, or SaaS expansion.

| Readiness area | Minimum standard before launch |

|---|---|

| Market thesis | A clear reason Bahrain is the right first or next GCC market |

| Buyer | One named buyer type, one painful workflow, and one budget owner |

| Regulated activity | A mapped view of whether the product touches money, credit, investment, payments, digital assets, identity, or financial data |

| MVP scope | The first version includes the trust features needed for testing, not only the visible feature set |

| Compliance | AML/CFT, customer disclosure, data protection, confidentiality, complaints, and audit assumptions reviewed |

| Banking and APIs | Required bank accounts, payment rails, open banking, KYC, or compliance integrations identified |

| Security | Role permissions, logs, monitoring, secure hosting, incident process, and access controls planned |

| Localization | Arabic, English, support hours, onboarding expectations, contracts, and buyer norms reviewed |

| Program fit | EDB, CBB sandbox, Bahrain FinTech Bay, Tamkeen, studio, or fund route selected by risk reduction |

| GCC expansion | What changes for Saudi Arabia, UAE, Qatar, Kuwait, or Oman is documented |

If several rows are vague, slow down. Bahrain rewards focused founders, but it exposes weak product thinking quickly when the product touches money, data, or institutional trust.

What founders should build first

For fintech founders, build the trust layer before the growth layer. That means onboarding, KYC assumptions, customer-money flow, ledger logic, reconciliation, bank integrations, audit logs, complaints, and compliance reporting.

For SaaS founders, pick a department and a workflow. “Bahrain SaaS” is too broad. Finance operations, compliance, procurement, HR, customer service, education administration, healthcare operations, logistics, and SME finance all have different buyers and risk thresholds.

For AI founders, avoid the generic assistant pitch. Build a controlled workflow with human review, source visibility, permissions, audit logs, and measurable time savings. In regulated or enterprise environments, the buyer wants to know what the system does when it is wrong.

For Islamic finance and Shariah-compliant products, build around governance and evidence. The product should make approvals, product rules, reporting, customer disclosure, and exception handling easier for the institution, not only more convenient for the end user.

For cybersecurity and compliance startups, Bahrain’s financial-services concentration can be useful, but only if the product fits a real operational problem: account takeover, phishing response, brand protection, third-party risk, audit evidence, data access, transaction monitoring, or incident readiness.

The founder takeaway

The Bahrain startup ecosystem is strongest for founders who need a serious but manageable place to build regulated, fintech, B2B, or enterprise-trust products for the GCC. Its value is not hype. It is focus: financial services depth, a visible CBB sandbox, Bahrain FinTech Bay, Bahrain EDB, Tamkeen, venture studios, regional cloud infrastructure, and a cost base that can extend runway.

The tradeoff is that Bahrain does not let founders hide from product risk. If the product touches money, data, security, or institutional workflows, the MVP has to carry more trust from day one.

That is the right lesson for GCC founders. Use Bahrain to make the product sharper: clearer buyer, cleaner compliance assumptions, better architecture, stronger onboarding, safer data handling, and a more believable expansion path.

The real opportunity in the Bahrain startup ecosystem is not just launching from Manama. It is building a product that can earn trust in Bahrain and then carry that proof into the wider GCC.