The UK startup ecosystem in 2026 is strong, but it is not easy money. Capital is flowing into AI, fintech, SaaS, healthtech, govtech, and climate tech. At the same time, investors, public buyers, and enterprise customers are asking harder questions about compliance, product evidence, infrastructure cost, and speed from prototype to production.

That makes the UK attractive for founders who can turn policy momentum into usable products. It is less forgiving for teams that mistake market attention for product readiness.

The headline case is clear. Dealroom reported that UK startups raised $17.1 billion in the first six months of 2026, with full-year funding on track for $34.2 billion if the pace continues. The same dataset shows $23.7 billion raised in 2025 and a UK startup enterprise value of $1.4 trillion. The opportunity is real, but the pattern is concentrated: the largest AI and infrastructure rounds are absorbing attention while mid-stage companies still need stronger evidence to raise.

For founders and scaleups, the practical question is not “Is the UK a good market?” It is: where does the UK give us an unfair product advantage, and can we execute quickly enough to use it? The broader startup funding trends for 2026 explain why strong market totals do not make capital evenly available, while Hapy’s AI product development guide covers the path from prototype attention to production trust.

Why the UK Startup Ecosystem Still Matters

The UK startup ecosystem still matters because it combines four advantages that rarely sit in one market: deep venture capital, world-class universities, a sophisticated financial system, and a public sector that is now explicitly trying to become a better buyer of AI and digital products.

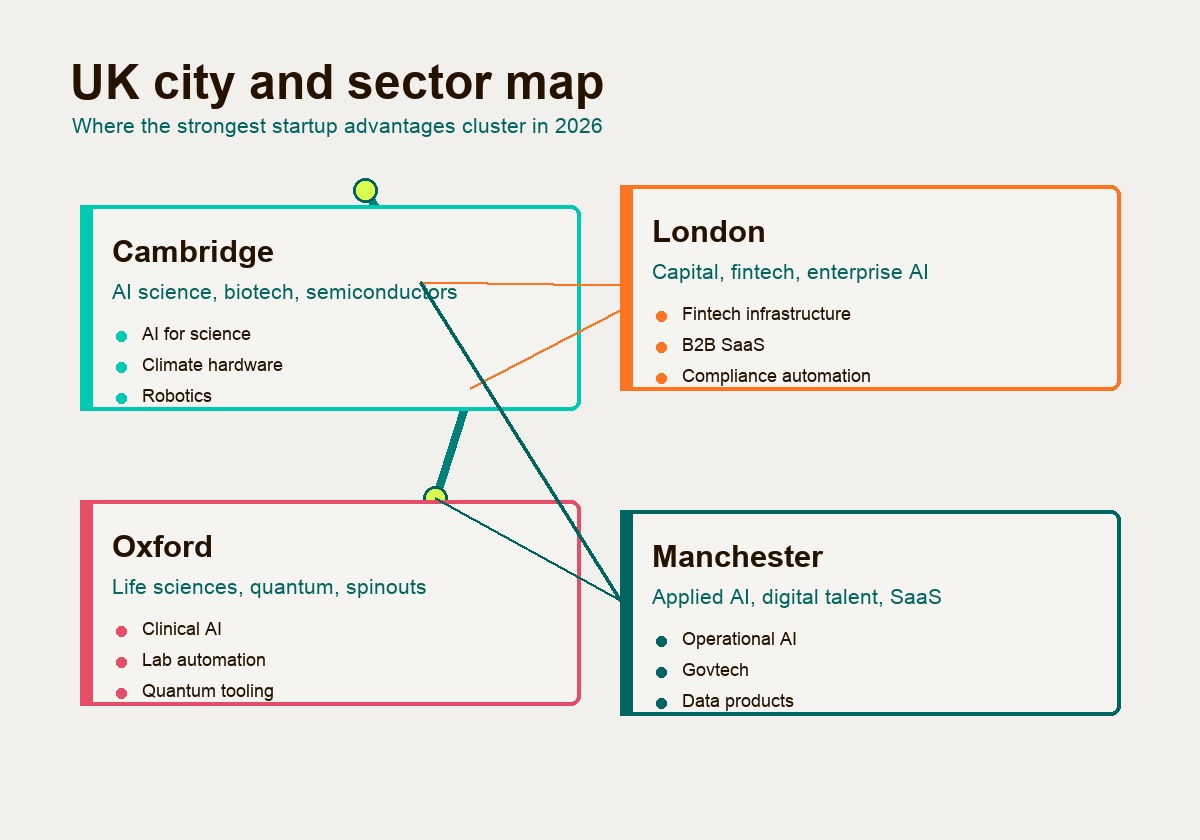

London remains the centre of gravity. Dealroom’s UK tracker shows London-led startup funding at $26.2 billion over the 12 months to the end of Q2 2026, followed by Cambridge at $3.0 billion, Oxford at $705 million, and Manchester at $199 million. London also remains the strongest commercial base for fintech, enterprise SaaS, AI, and venture capital.

But the UK is not only London. Cambridge and Oxford provide science, IP, and deeptech company creation. Manchester is becoming the most credible northern scaleup base for applied AI, B2B SaaS, fintech, and digital infrastructure. For founders, the best city choice depends less on brand and more on which advantage the product needs most: capital access, regulated buyers, scientific talent, enterprise customers, or lower operating friction.

| City cluster | Strongest advantage | Best-fit product opportunities | Founder risk to manage |

|---|---|---|---|

| London | Capital, customers, fintech, enterprise buyers | Fintech infrastructure, AI workspaces, B2B SaaS, compliance automation | High costs and crowded categories |

| Cambridge | Research depth, AI science, biotech, semiconductors | AI for science, climate hardware, healthtech, materials science, robotics | Long R&D cycles and specialist hiring |

| Oxford | Life sciences, quantum, fusion, university spinouts | Clinical AI, diagnostics, lab automation, quantum tooling | Clinical proof, IP terms, procurement time |

| Manchester | Applied AI, digital talent, fintech, SaaS | Operational AI, B2B SaaS, civic tech, data products | Smaller funding pool and buyer concentration |

AI Policy Is Creating a Product Window

The AI Opportunities Action Plan is the clearest policy signal in the UK market. Published by the Department for Science, Innovation and Technology in January 2025, the plan sets out 50 recommendations to grow the UK AI sector, increase adoption across the economy, and improve products and services.

The most useful point for founders is not the policy language. It is the buying signal. The plan pushes the UK toward three product markets:

- AI infrastructure, including sovereign compute, AI Growth Zones, energy-aware data centres, and secure model operations.

- AI adoption in public services, especially where pilots can move into evaluated, governed deployment.

- Homegrown AI capability, where the UK wants stronger domestic companies at more layers of the AI stack.

The compute piece is especially important. The action plan recommends expanding the AI Research Resource by at least 20x by 2030 and establishing AI Growth Zones to accelerate AI data centre buildout. That creates demand for tooling around model deployment, audit trails, data governance, energy optimisation, and secure operations.

For AI founders, this changes the product brief. “We use AI” is not enough. A stronger UK AI startup can answer:

- Which regulated workflow are we improving?

- What data rights, safety case, and audit trail does the buyer need?

- How does the product reduce labour, risk, cost, delay, or energy use?

- Can we move from pilot to production without rewriting the architecture?

That last point is where many UK AI startups will win or lose. The market has no shortage of demos. The shortage is production systems that satisfy security, procurement, compliance, integration, and user adoption at the same time.

Funding Momentum Is Real, But Selective

UK venture capital has momentum, but founders should read the numbers carefully. Dealroom’s 2026 UK data shows a record opening half, while its stage breakdown shows capital concentrating heavily in scaleup rounds of $100 million or more. The UK is raising more money, but not every founder has more room to manoeuvre.

The operating environment is also more complicated than the funding charts suggest. In March 2026, techUK and Public First polling found that 56% of tech firms described the UK environment as challenging for expansion, and 45% had considered relocating investment or operations outside the UK. That does not cancel the opportunity. It means founders need sharper product choices and fewer vague bets.

That pattern is reinforced by domestic capital reform. The British Business Bank’s British Growth Partnership is designed to help pension funds allocate more capital into UK venture. Its first fund announced a GBP 200 million first close on April 1, 2026, backed by Aegon UK, NatWest Cushon, and M&G. The direction is useful for scaleups, but it does not remove the need for product evidence.

Early-stage founders should expect investors to ask for:

- A tighter customer segment

- Clear retention or repeat-use evidence

- A visible path to revenue quality

- A realistic view of technical debt

- Compliance assumptions tested before enterprise sales

- A product roadmap connected to funding milestones

This is why UK startups should treat capital as an accelerator, not as the strategy. A stronger funding story starts with product proof: a buyer problem, a working wedge, a measurable outcome, and a credible build path. Hapy’s guide to SaaS product-market fit is useful here because it separates traction from durable fit.

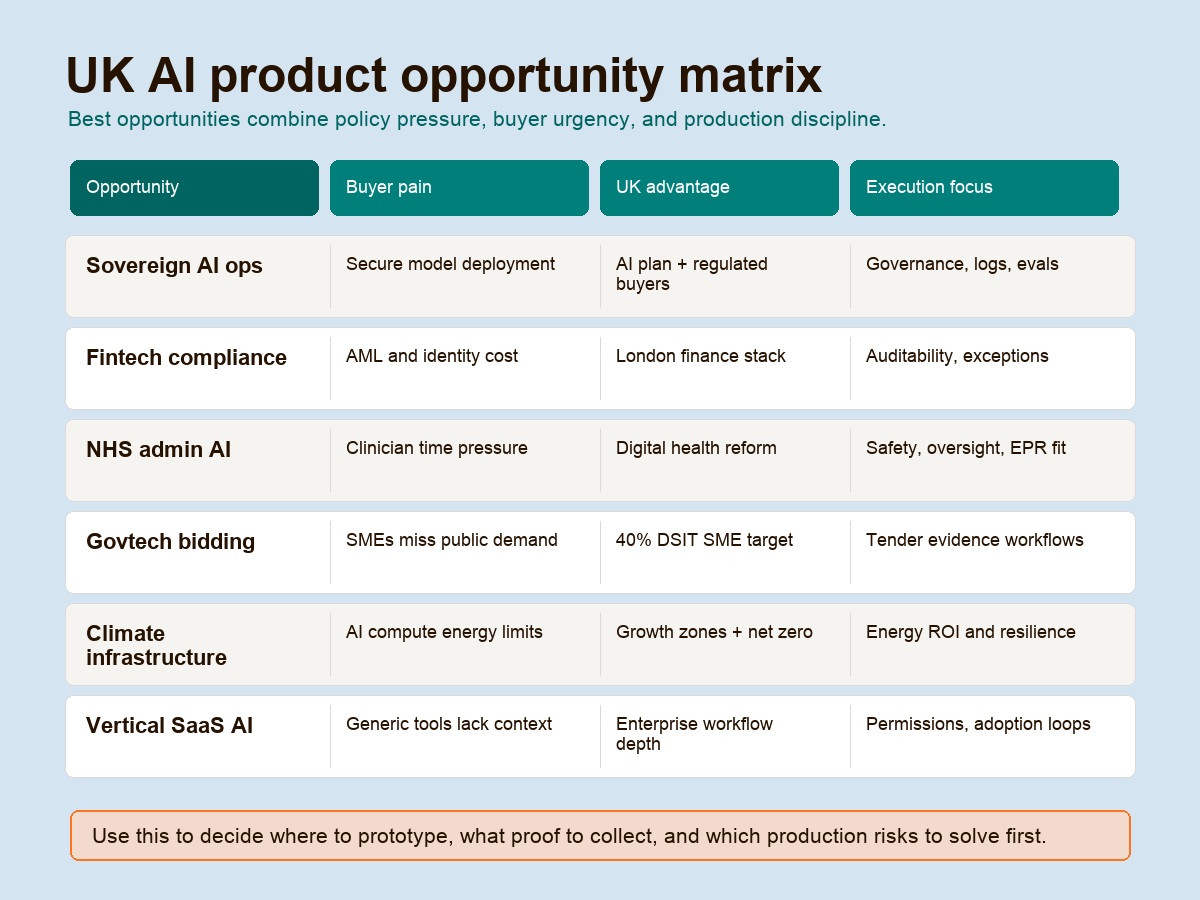

UK AI Product Opportunity Matrix

The best UK AI product opportunities sit where policy pressure, buyer urgency, and technical feasibility overlap. The founders most likely to benefit are not only the teams building frontier models. They are also the teams turning AI into boring, reliable workflow infrastructure for regulated markets.

| Opportunity | Buyer pain | Why the UK is a good testbed | Product execution requirement |

|---|---|---|---|

| Sovereign AI operations | Public and regulated buyers need secure AI deployment, audit trails, and data residency | AI policy, public-sector demand, and regulated industries are moving together | Governance, logging, access control, red-team process, model evaluation |

| Fintech compliance infrastructure | AML, fraud, onboarding, identity, and cross-border controls remain expensive | London has banks, fintechs, regulators, and enterprise buyers in one market | Low-latency integrations, explainability, false-positive management |

| NHS admin automation | Clinicians and admin teams need time back before clinical AI can scale | The 10 Year Health Plan pushes the NHS from analogue to digital and toward AI-enabled care | Clinical safety, human oversight, workflow integration, procurement patience |

| Govtech bidding and compliance | SMEs struggle to find, qualify for, and respond to public opportunities | DSIT has a 40% SME procurement spend target for 2025 to 2028 | Tender intelligence, policy mapping, evidence packs, compliance workflows |

| AI-enabled climate infrastructure | Data centres and industry need lower energy cost and better grid resilience | AI Growth Zones and net-zero pressure create direct demand | Hardware/software integration, energy data, ROI proof, regulatory readiness |

| Vertical B2B SaaS workspaces | Teams need AI inside the workflow, not as a separate chatbot | UK has strong enterprise SaaS, fintech, professional services, and applied AI buyers | Workflow depth, data permissions, adoption loops, integration quality |

Sector Opportunities For UK Startups

Fintech: Infrastructure Beats Consumer Novelty

UK fintech startups still benefit from London’s banking depth, open banking history, and capital markets expertise. But the stronger 2026 opportunity is infrastructure: compliance, identity, fraud, payments operations, treasury, SME lending workflows, and embedded finance controls.

The British Business Bank reported that gross SME bank lending increased to GBP 68 billion in 2025, and that challenger and specialist banks accounted for 60% of gross SME bank lending. That matters because fintech demand is no longer only consumer apps and challenger current accounts. It is the operational layer underneath lending, risk, onboarding, and business finance.

The product opportunity is to make regulated finance faster without making risk teams nervous. Founders should design for auditability, explainability, human review, and exception handling from the start.

Healthtech: Start With Admin, Then Earn Clinical Trust

The UK healthtech opportunity is large because the NHS is under pressure and explicitly trying to modernise. The 10 Year Health Plan for England sets out three shifts: hospital to community, analogue to digital, and sickness to prevention. Its executive summary says the plan aims to make the NHS “the most AI-enabled care system in the world.”

For founders, the near-term opportunity is not to replace clinicians. It is to remove administrative drag, improve access, reduce missed appointments, support triage, and make care pathways more visible.

Healthtech teams should assume clinical safety and procurement friction from day one. Products touching clinical workflows need safety cases, clear human oversight, data protection, integration planning, and evidence that the tool improves outcomes or releases capacity.

Govtech: Procurement Reform Creates a New Wedge

Govtech is becoming more founder-friendly because the UK is trying to lower procurement friction for smaller suppliers. DSIT’s SME Action Plan for 2025 to 2028 commits to a target of 40% of procurement spend with SMEs and points to demo-based procurement, simplified templates, and an Innovation Marketplace.

That creates two kinds of opportunity. The first is for startups selling into government. The second is for startups helping other SMEs sell into government: tender matching, bid drafting, compliance evidence, supplier onboarding, social value documentation, and public-sector sales intelligence.

The constraint is still trust. Govtech founders should build products that make procurement officers’ lives easier, not just products that tell startups where tenders exist.

B2B SaaS: Vertical AI Needs Workflow Ownership

UK SaaS startups have a good market if they solve expensive work in finance, professional services, healthcare, logistics, insurance, energy, construction, or government. The weak version is a generic AI assistant. The strong version owns a workflow, understands the data model, and creates evidence that the customer can use.

For UK SaaS founders, the question is whether AI improves a measurable process: faster underwriting, fewer missed compliance tasks, shorter reporting cycles, cleaner onboarding, better project visibility, lower support burden, or faster product delivery.

The build risk is technical debt. AI features often move quickly in prototype and then become hard to operate when permissions, latency, monitoring, data retention, and customer-specific workflows arrive. Hapy’s guide to technical debt cost in 2026 is relevant because the tax appears exactly when a team tries to scale.

Climate Tech: Compute And Energy Are Now Connected

Climate tech is no longer separate from AI infrastructure. If the UK expands compute capacity, it will need better power planning, cooling, grid flexibility, waste-heat reuse, and energy-aware scheduling. That gives climate startups a practical buyer path: reduce the cost and constraint of AI infrastructure.

The UK opportunity is not only carbon accounting. It is operational climate software and hardware that helps data centres, industrial sites, universities, hospitals, and local authorities lower energy cost while keeping systems reliable.

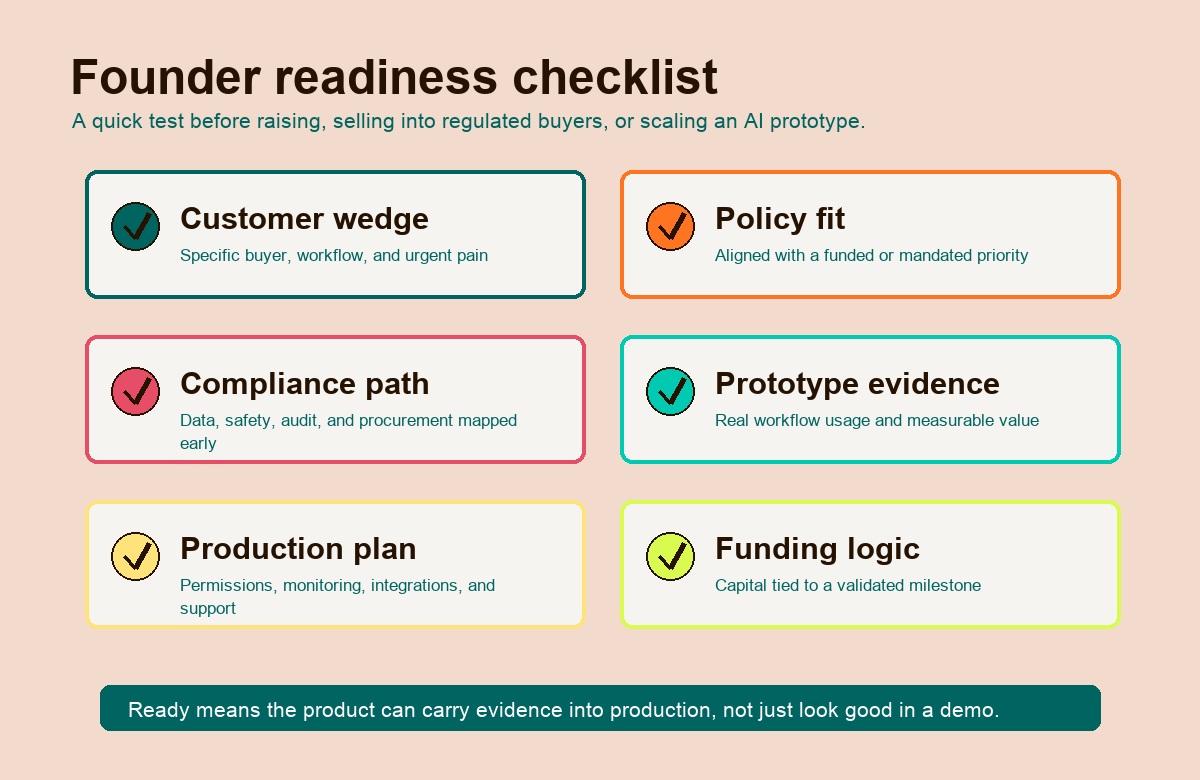

Founder Readiness Checklist

Founders should use the UK market’s momentum as a forcing function. Before raising, applying to an accelerator, or selling into regulated buyers, pressure-test the product in six areas.

| Readiness area | What good looks like | Red flag |

|---|---|---|

| Customer wedge | A specific buyer, workflow, and urgent pain | ”Everyone in finance/health/government” |

| Policy fit | The product aligns with a funded or mandated priority | The policy reference is only a slide-deck claim |

| Compliance path | Data, safety, audit, and procurement assumptions are mapped early | Compliance is left for enterprise sales |

| Prototype evidence | Users complete a real workflow and measurable value appears | Demo praise without usage depth |

| Production plan | Architecture supports permissions, monitoring, integrations, and support | Prototype stack would need a rebuild |

| Funding logic | Capital accelerates a validated learning or scaling milestone | Raise size is based on market excitement |

This checklist matters because the UK market rewards credibility. A founder selling into an NHS trust, local authority, bank, insurer, or enterprise buyer cannot rely on speed alone. The product has to move fast and carry evidence with it.

What Founders Should Build Next

The strongest UK startup opportunities in 2026 are not generic AI products. They are AI-enabled systems that fit real buyer constraints:

- Compliance-native fintech infrastructure

- NHS and care workflow automation

- Public-sector procurement and delivery tooling

- Vertical SaaS for regulated professional workflows

- Energy-aware AI infrastructure and climate operations

- AI governance, monitoring, and evaluation platforms

The common thread is prototype-to-production execution. Founders need to identify the wedge, ship the narrow product, prove the outcome, then harden the system for the buyer’s real environment. That means compliance, integrations, user permissions, monitoring, data handling, and support are product decisions, not back-office details.

If you are building in the UK startup ecosystem, the market is giving you more than one tailwind: AI policy, capital reform, public-sector demand, university spinouts, fintech maturity, and regional tech hubs. The winning teams will be the ones that convert those tailwinds into a product a buyer can trust, deploy, and expand.

Hapy helps founders and scaleups move from idea and prototype into production-ready software. If your UK startup is trying to turn AI, SaaS, fintech, healthtech, or govtech momentum into a product roadmap, start with the problem, the proof, and the production path.