The Finland startup ecosystem is unusually strong at technical invention. Its founder problem is usually commercial translation.

Finland has deep engineering talent, a mature gaming sector, high AI adoption, research-heavy health and education technology, and specialized regional hubs in Helsinki, Oulu, and Tampere. It also has a small home market, conservative early customers, and founder frustration around culture, taxation, procurement, and scaling conditions.

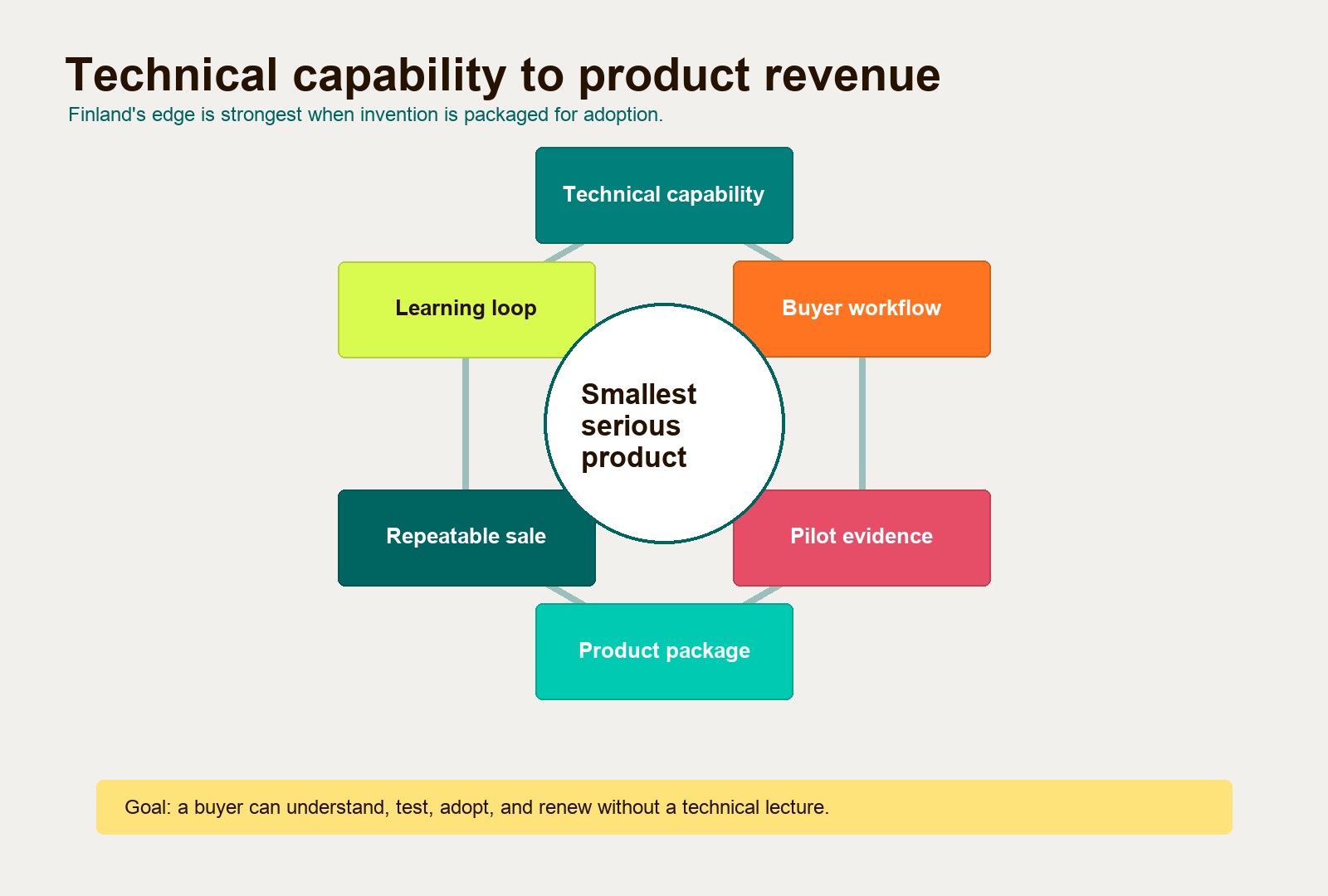

For European founders, the practical question is not whether Finnish startups can build difficult technology. They can. The better question is whether a Finnish technical advantage can be packaged into a product a buyer understands, trusts, pilots, and eventually buys without needing the founder in every meeting.

That is the angle to take into Finland in 2026: build from technical depth, but validate the commercial surface early.

For a broader Nordic read, compare this with the Denmark startup ecosystem and Sweden startup ecosystem guides. Denmark is stronger when public-sector trust, health, and climate deployment matter; Sweden is stronger when fintech, climate, and product-led SaaS density shape the expansion path.

Finland startup ecosystem in 2026: the useful read

Finland is a high-output startup market for its size. The 2025 Startup Study from Tesi, the Finnish Startup Community, and the Finnish Venture Capital Association identified more than 4,000 startup-origin companies founded since 2010. The same study says Finnish startup-origin companies generate about EUR 12 billion in annual revenue and employ close to 50,000 people worldwide.

The headline is encouraging, but the operating signal is more nuanced. New startup formation peaked at 584 launches in 2020 and has slowed to roughly 270 per year after 2021. That does not mean the ecosystem is weakening. It means Finland’s value is increasingly coming from companies that survive long enough to scale, not only from a large number of new experiments.

The same report says Finnish startups are increasingly powered by international talent, with more than a quarter of startup employees having a foreign background and nearly 40% in scaleups by 2022. Women make up roughly 30% of the startup workforce, with higher representation in scaleups. For founders, those numbers matter because Finland’s talent story is not only local engineering supply. It is also immigration, family integration, compensation, and whether a growing company can attract specialists into a small market.

The founder takeaway is simple: Finland is a strong place to build serious products, but a weak place to hide behind technical complexity. A deep product still needs a narrow buyer, a clear workflow, and evidence that the market wants the outcome.

Helsinki startup ecosystem: density, Slush, and scaleup gravity

The Helsinki startup ecosystem is Finland’s commercial center of gravity. It concentrates investors, operators, international founders, startup campuses, government-facing networks, and the soft-landing infrastructure that helps companies move from invention to market.

The Helsinki Startup Report found that Helsinki-based startups invested EUR 345 million in R&D in 2023, with about 3,000 R&D workers and roughly 330 doctoral-level researchers. That is a serious technical base for a city of Helsinki’s size. It also creates a practical tension: startups compete with universities, research institutes, and large companies for advanced technical talent.

Maria 01 is part of that density. Its 2025 impact report says the campus had 228 startups and 1,985 members in 2025, representing more than 40 nationalities. Its startups and alumni secured EUR 337 million in funding during the year, and 42% of active startups had at least one founder with an international background.

Slush gives Helsinki a second advantage: it turns the city into a capital and relationship node once a year. For Slush 2026, Innovate UK describes a Helsinki market visit linked to the conference, with the main event on November 18-19 and a “Bet on Europe” theme. The program says Slush 2026 expects more than 3,300 investors and 5,800 startup founders, with specific GBIP focus areas around video games, advertising technology, and marketing technology.

That matters commercially. Slush is not only a stage for fundraising announcements. It is a forcing function for founder packaging. If a product cannot be explained to investors, partners, and buyers in a noisy, time-compressed environment, the product story probably needs work.

For Helsinki founders, the product discipline is:

| Area | What Helsinki gives you | What founders still need to prove |

|---|---|---|

| Capital access | Investor density, Slush, Maria 01, operators, public funding routes | Milestones tied to customer evidence, not only technical progress |

| Talent | Advanced R&D workers, international founders, experienced scaleup alumni | Hiring plan, compensation logic, immigration readiness, leadership depth |

| AI and SaaS | Enterprise buyers, product teams, technical SaaS history | Workflow ownership, onboarding quality, permissions, and retention signals |

| Gaming and creative tech | Studios, tools, publishing know-how, Slush-adjacent attention | Scalable platform or service model, not only content or a prototype |

| Deep tech | VTT, Aalto, Otaniemi, research links, defense and quantum adjacency | Commercial path from lab proof to buyer adoption |

Helsinki is useful when the product needs capital, visibility, and cross-border relationships. It is less useful if the company has not decided who buys, why now, and what proof would make a cautious customer say yes.

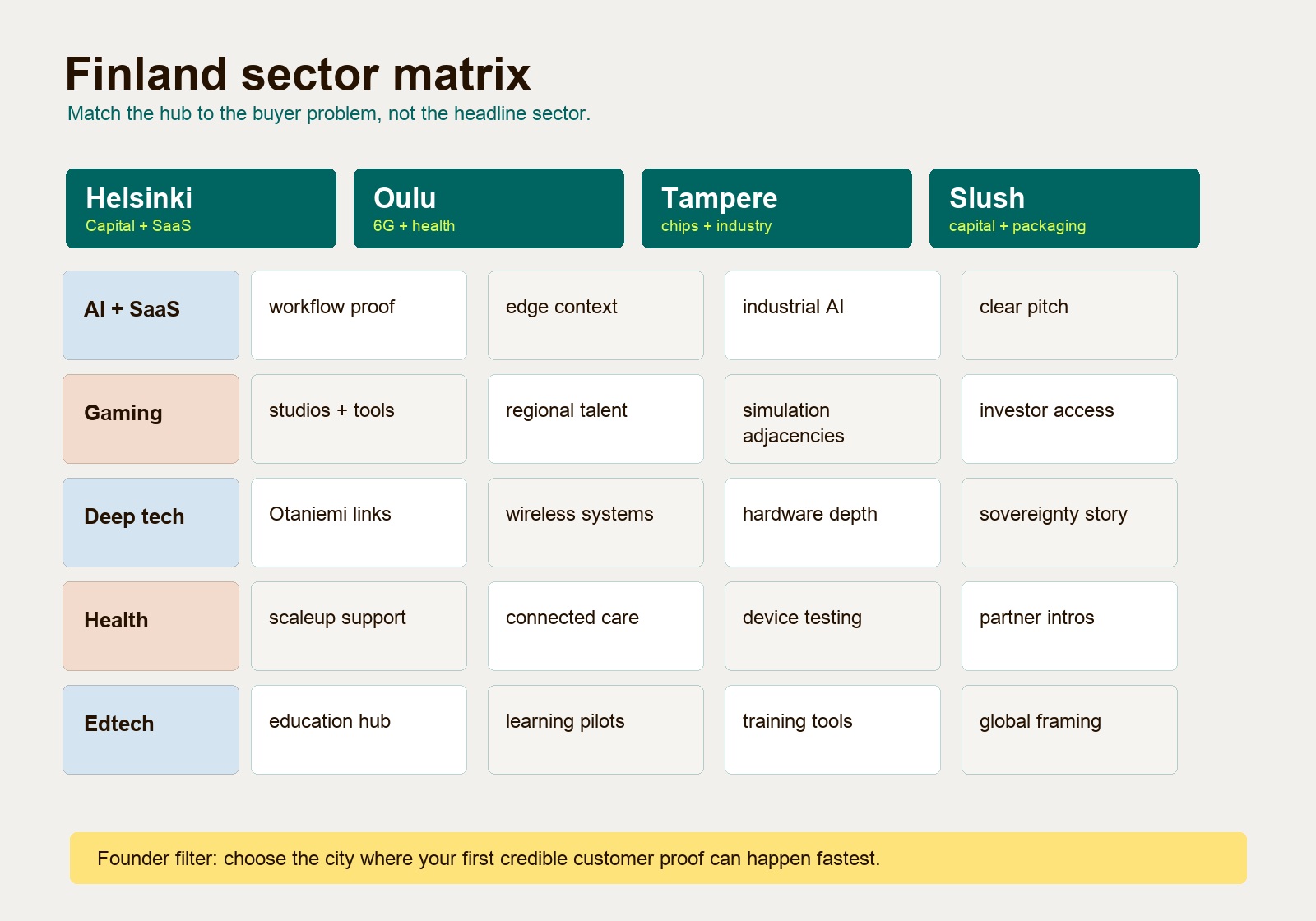

Oulu and Tampere: technical hubs with different buyer logic

Finland’s startup strength is not only in Helsinki. Oulu and Tampere are important because they show how regional technical depth can become product opportunity.

Oulu: wireless, connected health, and test environments

Oulu is one of Finland’s clearest examples of post-Nokia capability turning into a startup asset. The University of Oulu’s 6G research profile describes work on 6G solutions for a data-driven society, and the wider Oulu cluster links wireless, edge systems, software-defined networks, health technology, and testing infrastructure.

That combination matters because many future products will sit between connectivity and regulated user contexts: remote monitoring, hospital workflows, digital diagnostics, wearables, elder care, industrial safety, logistics, and defense-adjacent communications.

OuluHealth Labs adds a commercialization layer. The city describes OuluHealth Labs as a co-creation and testing environment for health and welfare products, giving companies access to real or simulated healthcare and social care settings. For founders, that is valuable because healthtech does not become credible through a polished app alone. It needs workflow fit, user feedback, data handling, clinical or care-context evidence, and procurement readiness.

Tampere: semiconductors, photonics, imaging, and industrial depth

Tampere is different. It is strongest where software touches hardware, manufacturing, imaging, semiconductors, photonics, and industrial systems. Invest in Tampere positions the region as one of Europe’s advanced hubs for semiconductor design, photonics, and imaging, citing more than 52,000 high-tech professionals in the region and more than 15,000 specialists across electrical engineering, chips, photonics, electronics, and materials science.

That makes Tampere relevant for founders building chips, imaging systems, industrial AI, test automation, robotics, defense-adjacent hardware, and manufacturing software. But it also raises the product bar. A hardware-heavy product cannot be sold with the same proof package as a lightweight SaaS tool. Buyers will ask about reliability, supply chain, test coverage, certification path, integration, lifecycle support, and who owns field failure.

Use Oulu when the product benefits from wireless, connected health, and applied testbeds. Use Tampere when the product depends on advanced hardware, industrial customers, and deep engineering talent. Use Helsinki when the company needs capital density, commercial packaging, and international startup visibility.

Finland sector matrix: where the opportunity is strongest

Finland’s strongest sectors share a pattern: technical depth is high, but the buyer often needs help translating that depth into a usable product, business case, and adoption path.

| Sector | Finnish strength | Product opportunity | Main commercialization risk |

|---|---|---|---|

| AI and Finnish SaaS | High enterprise AI adoption, strong engineering, B2B product companies | Workflow copilots, decision support, AI operations, data quality, vertical SaaS | Generic AI features without measurable workflow impact |

| Gaming and creative tech | Mature studios, mobile history, PC and cross-platform momentum | Game tooling, publishing infrastructure, community systems, monetization analytics | Building content when the scalable business is a platform or service |

| Deep tech and quantum-adjacent systems | Research institutions, VTT, Otaniemi, Tampere hardware depth | Specialized hardware, simulation, sensing, cryogenic systems, security, industrial software | Long sales cycles, unclear buyer, weak packaging around technical proof |

| Healthtech and connected care | OuluHealth, hospital testbeds, wearables, diagnostics, Finnish health data culture | Remote monitoring, care workflow tools, diagnostic support, patient operations | Clinical workflow, privacy, reimbursement, procurement, and evidence gaps |

| Education technology | Education reputation, research-led pedagogy, Helsinki Education Hub | Evidence-backed learning tools, assessment, teacher workflows, AI-assisted learning support | Edtech products that look engaging but do not prove learning value |

| Defense, space, and dual-use | NATO membership context, VTT DIANA, communications, earth observation, cybersecurity | Resilient communications, sensing, satellite data products, secure infrastructure | Procurement complexity, export controls, field validation, dual-use positioning |

| Climate and circular economy | Forests, energy systems, materials, circular economy, industrial efficiency | Carbon data, industrial efficiency, materials tracking, recommerce infrastructure | Sustainability claims without verifiable data or buyer ROI |

The pattern is consistent: Finland can produce difficult technology, but founders need to make the buying case simpler than the engineering.

Gaming, AI, and SaaS: mature markets need sharper packaging

Finland gaming startups have a mature support system and a global reputation, but the market has changed. PocketGamer.biz reported in April 2026 that Finland’s active studio count had risen to 270 studios, up 15% in two years, while 75 new startups emerged over three years. The same article notes that mobile remains dominant among established companies, but early-stage studios are moving into PC, console, web, and cross-platform development, with more than 70% of games released in 2024 available on PC.

That is not only a gaming story. It is a product strategy lesson. Mature sectors force teams to find new distribution, new tooling, and new business models when the old wedge becomes crowded. For a Finnish game studio, the product opportunity may be a tool, publishing system, analytics layer, community engine, user acquisition platform, or live-ops workflow rather than another content bet.

The same logic applies to Finland AI startups and Finnish SaaS. AI Finland reports that 66% of Finnish companies use generative AI, the highest share among EU countries on its page, while 85% of technology industry companies say they are investing in AI. High adoption is good, but it also means buyers become more skeptical of thin AI wrappers. If everyone can demo a model, the commercial edge moves to data access, process integration, controls, and measurable outcomes.

For Finnish SaaS founders, the product questions should be direct:

- What workflow does the product own after onboarding?

- What before-and-after metric proves value?

- What existing system does it replace, extend, or connect?

- What risk does it reduce for the buyer?

- What part of the product would be hard for a competitor to copy in three months?

If the answer is mostly “we use AI” or “we have better engineers,” the package is not ready. Hapy’s guide to a SaaS business model is a useful next step when pricing, retention, expansion, and product packaging still feel soft.

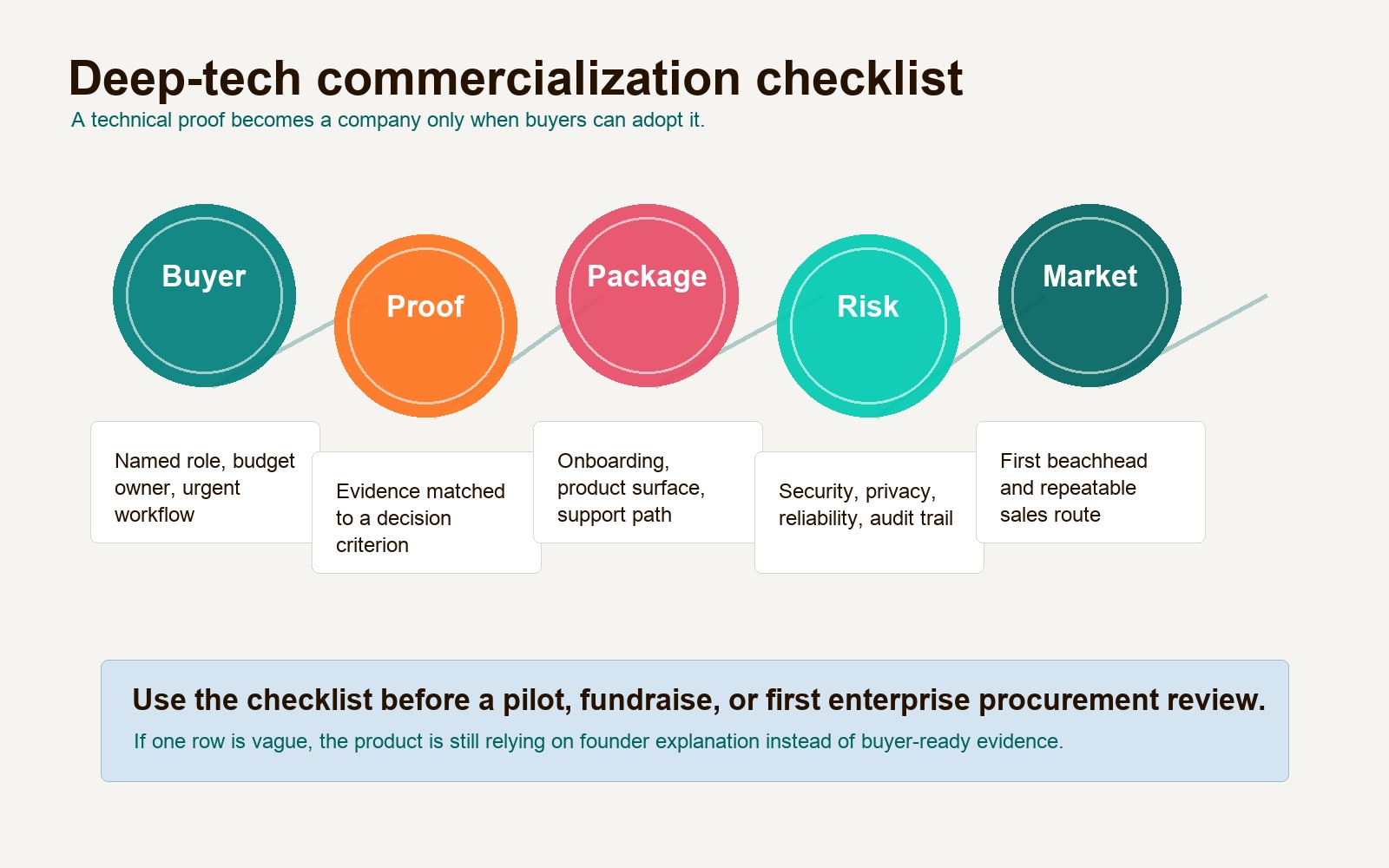

Deep tech commercialization checklist

Finnish deep tech founders should treat commercialization as part of product development, not as a later sales layer. A technical proof is not the same thing as a product. A product is the repeatable package that lets a buyer adopt the proof without rebuilding the company around it.

Use this checklist before raising around a technical milestone or entering a major pilot.

| Readiness area | Minimum evidence before scaling |

|---|---|

| Buyer | One named buyer role, budget owner, and urgent workflow |

| Use case | A specific job where the product changes cost, speed, risk, quality, revenue, or compliance |

| Proof | Lab, simulation, prototype, pilot, or deployment evidence matched to the buyer’s decision criteria |

| Packaging | A buyer-facing product surface, onboarding path, success metric, and support model |

| Integration | Clear fit with the buyer’s existing data, hardware, identity, procurement, or operational stack |

| Risk controls | Security, privacy, reliability, audit logs, failure handling, and human oversight where needed |

| Commercial model | Pricing tied to buyer value, not only R&D cost or technical novelty |

| Procurement | Documents a cautious enterprise, hospital, public buyer, or industrial customer can review |

| International path | First beachhead market, export constraints, partner model, and support coverage |

| Learning loop | Pilot acceptance criteria, feedback cadence, and decision rule for what gets built next |

This is especially important in dual-use, defense, health, semiconductors, education, and AI. VTT’s first NATO DIANA accelerator in Finland shows how serious the dual-use route has become: the 2026 program selected companies working on advanced communications and gives each selected company EUR 100,000 in funding, with access to DIANA test centers and defense-market support. That is a strong validation environment, but it is still not a substitute for buyer-specific product work.

For AI-heavy products, Hapy’s article on the forward-deployed engineer role is relevant because many Finnish deep tech and AI products need someone who can turn a demo into production behavior inside a real customer workflow.

Health and education technology: evidence before scale

Finland’s health and education technology opportunity is strongest when founders respect evidence.

In healthtech, Finland has the right ingredients: technical talent, wearables history, Oulu’s connected-health infrastructure, hospital testbeds, and a population comfortable with digital services. But health products need proof in context. A remote monitoring tool, diagnostic assistant, or care operations platform has to fit real staff workflows, patient privacy, procurement, and clinical or care-quality standards. The product cannot rely only on a persuasive demo.

Education technology has a similar pattern. The Finnish Edtech Report 2025 says 270 edtech companies were active in 2023, and sector net sales rose from EUR 74 million in 2010 to EUR 290 million in 2023. It also notes that almost 84% of edtech firms are micro-enterprises, which means many companies still face the hard work of scaling beyond promising pilots.

That report’s most useful phrase is “pedagogy-first.” Finnish edtech is strongest when the product improves learning, teacher workflow, assessment, inclusion, or institutional operations in a way that can be explained and measured. AI can help, but it should not become a shortcut around learning science.

For founders, health and edtech both require a narrower product stance:

- Pick one user workflow before building a platform.

- Define the evidence a buyer or institution would trust.

- Test in a real environment, not only a founder-led demo.

- Package implementation so adoption does not depend on heroic support.

- Build privacy, consent, permissions, and reporting into the first serious version.

The commercial opportunity is not “Finland is good at health and education.” It is that Finland can produce products where evidence, trust, and technical execution are part of the brand.

Founder challenges: why technical talent is not enough

The Finland founder challenge is cultural and commercial as much as technical.

Slush’s Finnish founder survey reported that 53% of surveyed Finnish founders were considering or actively planning to relocate business operations abroad. The same survey says 56% identified general attitudes and culture as obstacles to startup growth, with other issues including taxation, small market size, and regulatory complexity.

That should not be read as a reason to avoid Finland. It should be read as a warning about validation design. If local corporate and public buyers are conservative, a founder cannot wait for Finland alone to validate the product. The company needs a deliberate design-partner strategy, likely with Nordic, EU, UK, or U.S. expansion built into the first commercial plan.

The small domestic market also changes MVP strategy. A Finnish MVP should not be the smallest possible demo for a few friendly users. It should be the smallest serious product that can survive an international buyer conversation.

That means:

- The product narrative must be simple enough for a non-technical buyer.

- The workflow must be narrow enough to test quickly.

- The pilot must have measurable success criteria.

- The team must know which market comes after Finland.

- The product must include the trust layer the target sector expects.

Hapy’s guide to a product strategy roadmap is useful here because Finland’s technical teams often need help sequencing what to build, what to validate, and what to delay until customer evidence supports it.

Product opportunities for European founders

The best Finland startup opportunities are not generic country-themed ideas. They are products that turn Finnish technical strengths into buyer-ready tools.

In AI and SaaS, build workflow-specific systems for finance operations, marketing intelligence, customer operations, supply-chain planning, developer productivity, cybersecurity, and public-sector processes. The product should show accuracy, permissions, auditability, and adoption metrics before it claims enterprise readiness.

In gaming, build around the business of games: creator tools, live-ops infrastructure, analytics, community, monetization, cross-platform tooling, and publishing support. Finland’s gaming reputation gives credibility, but the product still needs a scalable commercial wedge.

In deep tech, build the bridge from prototype to deployment: test automation, simulation, compliance evidence, hardware diagnostics, edge deployment, documentation, procurement packs, and model evaluation. These are not glamorous, but they are often the missing layer between research and revenue.

In healthtech, build care workflow tools that fit staff reality. The opportunity is not another wellness dashboard. It is a product that reduces clinical admin load, improves remote monitoring, supports diagnostics, or helps institutions coordinate care safely.

In edtech, build learning products with evidence. AI tutors, assessment tools, teacher workflow systems, and learning analytics can work when they respect pedagogy, privacy, and institutional adoption.

In defense, space, and dual-use, build for reliability, procurement, and field validation from the start. Finland’s security context creates demand, but buyers will not accept vague resilience claims.

The founder takeaway

The Finland startup ecosystem is strongest when technical capability becomes a product customers can buy. Helsinki gives founders capital density, Slush, international networks, and startup infrastructure. Oulu gives wireless, connected health, and testbed strength. Tampere gives semiconductors, photonics, imaging, and industrial depth. Gaming, AI, deep tech, health, education technology, and Finnish SaaS all have credible openings.

The harder truth is that Finland’s strengths can become founder traps. Deep engineering can hide unclear positioning. A respected research base can delay customer discovery. A strong local ecosystem can make a tiny domestic market feel larger than it is. A great demo can distract from procurement, onboarding, integration, and retention.

Founders should build the smallest serious product: narrow enough to validate, strong enough to earn trust, and packaged well enough that a buyer can understand the value without a technical lecture.

That is how Finland’s technical advantage turns into revenue.