The Sweden startup ecosystem rewards founders who can turn sharp product thinking into global execution. Stockholm gives the country unusual density: experienced operators, venture capital, fintech history, AI talent, design-led product culture, and alumni networks from companies such as Spotify and Klarna.

That does not make Sweden an easy market. It is small, direct, expensive, highly digital, and increasingly selective about capital. A weak MVP, vague positioning, or generic AI wrapper will be exposed quickly. The upside is that Swedish buyers and operators can be strong design partners when the product saves time, clarifies complexity, and feels usable from the first serious workflow.

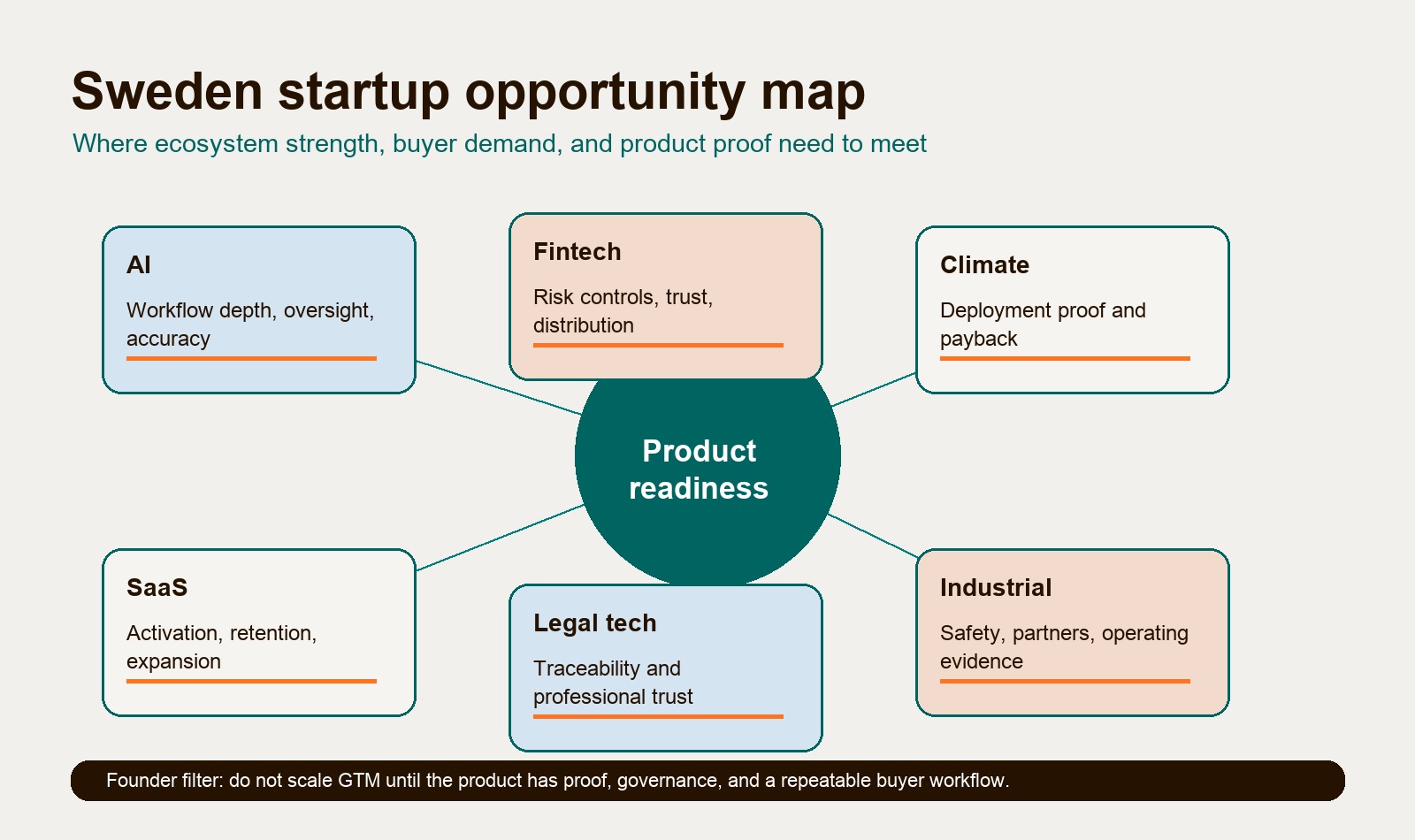

For European founders, the practical question is not whether Sweden is “good for startups.” It is. The better question is whether your company benefits from Sweden’s strengths: product-led software, fintech infrastructure, applied AI, climate and energy systems, legal automation, vertical SaaS, and Nordic expansion.

If you are comparing Nordic entry points, pair this with the Denmark startup ecosystem and Finland startup ecosystem guides. Denmark is useful for trust-heavy health, climate, and public-sector workflows; Finland is useful when the product depends on deep technical capability and commercialization discipline.

Sweden startup ecosystem in 2026: the useful read

Sweden is a mature startup market with a selective funding environment. Dealroom’s live Sweden profile shows Swedish startups raised $3.2 billion in venture capital in 2025, with $2.7 billion raised in the first five months of 2026 and a projected annualized path of $6.4 billion. It also lists 57 Swedish unicorns and a combined enterprise value of $236.4 billion for VC-backed Swedish startups founded since 1990.

Stockholm is the center of gravity. Startup Genome’s Stockholm profile reports a $56 billion ecosystem value for H2 2023 through 2025, $1.6 billion in early-stage funding, and $34 billion in exit value. Dealroom’s metro data puts Stockholm far ahead of other Swedish regions, with $2.9 billion in venture funding in 2025 and 35 Swedish unicorns tied to the metro.

The funding signal is important because it is not evenly spread. Dealroom shows that in the trailing four quarters through Q1 2026, 46% of Swedish startup capital went into scaleup rounds above $100 million, 31% into $15 million to $100 million breakout rounds, and 23% into rounds below $15 million. A founder should read that as a milestone discipline warning. Sweden has capital, but it wants evidence.

Stockholm startup ecosystem: product density over market size

The Stockholm startup ecosystem matters because it lets small teams build for large markets early. Sweden’s home market is too small to support lazy local monopolies, so stronger teams tend to build internationally from the beginning.

Spotify is the clearest cultural example. It turned Swedish product, engineering, licensing, and personalization discipline into a global audio platform. Just as important, its alumni network now recycles product judgment, capital, and operating habits into newer companies. That “Spotify alumni” effect is not magic. It means more founders have seen what scaled product systems, experimentation, recommendations, subscriptions, and international teams look like from the inside.

Klarna is the fintech example founders should study with nuance. Its September 2025 New York listing, which the AP reported raised about $1.37 billion at a $40 IPO price, showed the global reach of Swedish fintech. It also showed the pressure that follows scale: public-market scrutiny, credit risk, regulatory attention, and the need to move beyond a single BNPL wedge into broader consumer finance.

The lesson for founders is not “copy Spotify” or “copy Klarna.” It is that Swedish product culture tends to reward products that feel simple while hiding serious operational machinery underneath. The interface must be calm. The system behind it cannot be shallow.

Funding, sectors, and what Swedish investors are rewarding

Swedish startup funding in 2026 is strongest where the product has a credible moat: energy infrastructure, AI, fintech, legal automation, health, climate, advanced mobility, and vertical software. The broad reset after 2022 did not remove capital; it made investors more selective about what deserves it.

Tech.eu’s March 2026 review said Sweden raised EUR 4.1 billion in tech funding in 2025, ranking fifth in Europe, with capital concentrated in hardware, energy, data infrastructure, software, healthtech, AI, and cleantech. The same report highlights EcoDataCenter, Elvy, Lovable, Neko Health, Legora, Aira, Qvantum, Froda, and Einride as examples of where capital flowed.

That list is useful because it cuts across hype categories:

| Sector | Swedish wedge | What founders should prove |

|---|---|---|

| AI | Applied workflow systems, software-building tools, health, legal, data infrastructure | Accuracy, permissions, human oversight, integration, and measurable cycle-time reduction |

| Fintech | Payments, consumer finance, SME lending, embedded finance, compliance | Trust, risk controls, regulation, partner distribution, and clear unit economics |

| Climate tech | Heat pumps, energy storage, grid software, industrial decarbonization, sustainable data centers | Deployment proof, capex model, payback logic, and operational reliability |

| SaaS | Vertical workflows, product-led sales, collaboration, analytics, developer tools | Activation, retention, onboarding quality, expansion signals, and integration depth |

| Legal tech | AI-assisted research, drafting, review, patent workflows, compliance operations | Auditability, professional trust, source control, security, and liability boundaries |

| Mobility and industrial tech | Electric logistics, autonomy, manufacturing intelligence, robotics | Safety, fleet economics, hardware readiness, and partner operations |

The pattern is clear: Swedish startups can win with elegant product experience, but funding follows defensibility. Design is an advantage only when it helps a serious buyer adopt a serious system.

Climate tech after Northvolt: less mythology, more proof

Sweden climate tech is still attractive, but the Northvolt story changed how founders should talk about it. Northvolt was the flagship of European battery ambition, yet the company filed for bankruptcy in Sweden on March 12, 2025 after capital, supply chain, demand, and production ramp-up pressures converged.

The point is not that climate hardware is a bad market. It is that industrial climate products need more than a strong mission and a large TAM. They need manufacturing yield, supplier resilience, working capital planning, offtake confidence, quality systems, and a capital stack that matches the deployment timeline.

There is still underlying value in the assets and talent. In August 2025, Lyten entered a binding agreement to acquire Northvolt’s remaining assets in Sweden and Germany, including Northvolt Ett, Ett Expansion, Northvolt Labs, Northvolt Drei, and remaining IP. That is the more useful founder lesson: even when the original company fails, validated infrastructure, IP, and talent can remain strategically important.

For climate software and climate-adjacent SaaS, the opportunity is different. Founders do not need to build a factory to matter. Sweden has room for products that help enterprises manage energy demand, Scope 3 supply-chain reporting, building electrification, industrial maintenance, climate procurement, and grid-aware operations. The product bar is still high: buyers will expect evidence, not a prettier reporting dashboard.

AI, legal tech, and product-led SaaS

Sweden AI startups have an opening because the local culture is unusually friendly to digital products, but AI does not remove the need for product discipline. If anything, it raises the bar. A vague copilot is easy to demo and hard to keep.

The strongest AI products in Sweden are likely to sit inside narrow, high-value workflows: legal document review, patent operations, healthcare triage, developer tooling, customer operations, finance controls, data quality, procurement, and industrial planning. Legora and Lovable matter as examples because they connect AI to a visible product surface. One sells into a conservative professional workflow. The other turns natural language into software-building action. Both depend on UX trust as much as model capability.

The EU AI Act makes that trust more concrete. The European Commission explains that the AI Act entered into force on August 1, 2024, with prohibited practices applying from February 2025, GPAI obligations from August 2025, transparency rules from August 2026, and staged high-risk obligations after that. Founders building for employment, education, credit, healthcare, legal, public services, or critical infrastructure should treat AI governance as product scope, not legal clean-up.

SaaS founders should also be careful with product-led growth. Swedish product culture makes PLG attractive, but the old “free users first, sales later” playbook is weaker in mature B2B markets. Better Swedish SaaS motions combine product-led onboarding with sales-assisted expansion. The product identifies intent. Sales helps the account cross organizational, compliance, security, and integration barriers.

If your activation metric is only “created an account,” it is not enough. A Swedish or Nordic B2B buyer will care about whether the product reaches a useful workflow quickly, survives the handoff to a team, and keeps working once the first champion is no longer driving every step.

The Swedish product culture advantage

Swedish startups often punch above their market size because the product culture prizes restraint. The best products feel direct, calm, and easy to understand. That is not just an aesthetic preference. It is a commercial advantage when a company sells across languages, sectors, and countries.

The useful Swedish product principle is this: reduce the user’s cognitive load without hiding the system’s seriousness. A fintech product still needs risk controls. A legal AI product still needs traceability. A climate product still needs deployment economics. A SaaS product still needs permissions, onboarding, analytics, and integrations. The user should feel clarity, not simplification theater.

That creates a strong link between ecosystem culture and product execution:

| Cultural trait | Product implication | Risk if ignored |

|---|---|---|

| Direct communication | Clear positioning, honest onboarding, plain pricing logic | Vague messaging loses trust quickly |

| Design restraint | Fewer features, stronger defaults, cleaner workflows | Feature sprawl makes the product feel unserious |

| Global ambition | English-first product, international compliance, scalable support | A local-only MVP stalls after early pilots |

| Flat collaboration | Faster feedback loops with operators and design partners | Founder ego blocks useful critique |

| High digital trust | Buyers will try modern tools when risk is controlled | Weak privacy, security, or governance breaks adoption |

For founders, this means product design is not a layer added after strategy. It is how strategy becomes usable. Hapy’s guides to website usability testing and why users leave a website are useful if the product or marketing site is already leaking trust before a buyer can understand the value.

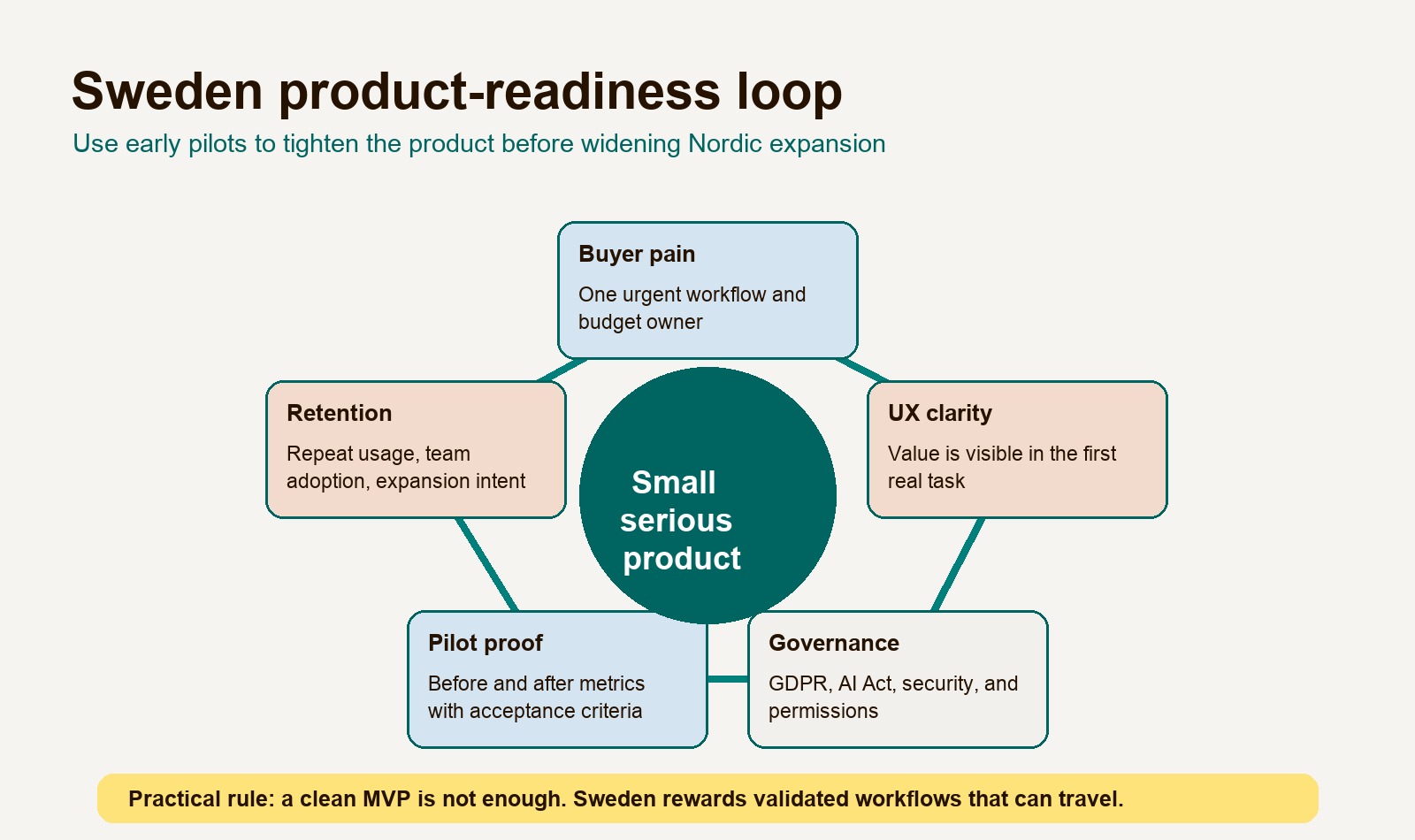

Sweden product-readiness checklist

Use this checklist before treating Sweden as an active launch or expansion market.

| Area | Minimum readiness standard |

|---|---|

| ICP | One named buyer role, one urgent workflow, and a clear budget owner |

| Product wedge | Specific job-to-be-done, not a broad “AI,” “fintech,” or “climate” claim |

| UX clarity | First-use experience shows the value without a long sales explanation |

| Evidence | Pilot plan with before/after metrics, acceptance criteria, and referenceable design partners |

| Compliance | GDPR baseline, AI Act exposure review, data processing terms, security evidence, and audit logs where needed |

| Integrations | CRM, finance, identity, legal, energy, ERP, data, or workflow integrations matched to the buyer’s stack |

| Pricing | Clear self-serve or pilot pricing logic, with enterprise path where procurement requires it |

| Team | Enough product, engineering, design, and customer success capacity to learn from pilots quickly |

| Nordic expansion | Clear view of what changes for Denmark, Norway, Finland, or broader EU buyers |

| Retention signal | Activation, repeat usage, team adoption, or workflow ownership measured before scaling sales |

If several rows are still vague, slow down. Sweden rewards efficient teams, but efficiency is not rushing. It is learning faster with less waste.

For SaaS founders, the next filter is product-market fit. Hapy’s guide to SaaS product-market fit signals can help teams separate promising usage from real readiness to scale.

Nordic sector opportunity table

Sweden can be a strong Nordic entry point, but the Nordics are not one uniform market. Use Sweden for the strengths it actually provides, then decide where the next proof should come from.

| Sector | Sweden | Denmark | Norway | Finland | Founder implication |

|---|---|---|---|---|---|

| Fintech | Stockholm payments, BNPL, embedded finance, SME lending | Banking partnerships, payments, insurance | Wealth, energy finance, compliance-heavy services | Digital public infrastructure and banking tech | Build trust, compliance, and partner distribution early |

| AI and SaaS | Product-led software, legal AI, developer tools, health AI | Life sciences, enterprise software, public-sector workflows | Energy, maritime, industrial operations | Developer tools, gaming, deep tech, cybersecurity | Pick a workflow where local proof travels |

| Climate tech | Heat pumps, batteries, grid software, sustainable data centers | Wind, agriculture, food systems, energy efficiency | Offshore energy, maritime, carbon management | Materials, circular economy, industrial efficiency | Match product evidence to physical deployment reality |

| Health and life sciences | Preventive health, digital care, medtech, AI triage | Pharma and biotech depth | Care delivery and public health systems | Diagnostics, health data, medtech | Validate privacy, clinical workflow, and reimbursement path |

| Industrial and mobility | Electric logistics, autonomy, manufacturing systems | Robotics, logistics, food production | Maritime, shipping, energy operations | Machinery, telecom, industrial software | Build for operational reliability before scale claims |

| Gaming and consumer products | Gaming, music, creator tools, design-led consumer UX | Lifestyle, subscriptions, marketplaces | Community and outdoor niches | Gaming and mobile expertise | Consumer products need global hooks from day one |

The Nordic opportunity is attractive because buyers are digitally mature and English-friendly. The trap is assuming that “Nordic” means frictionless. Procurement, language, regulatory expectations, labor rules, data hosting preferences, and partner networks can still vary by country.

Founder challenges to plan around

The first challenge is capital concentration. A market can show strong total funding while still being hard for early teams that do not have sharp proof. Founders should design milestones around buyer evidence, not presentation polish.

The second challenge is talent cost and mobility. Sweden has strong technical and product talent, but senior people are expensive and global hiring can run into work-permit rules. Verksamt’s 2026 law-change summary notes new work permit rules from June 1, 2026, including salary, insurance, and sector exemption details. Teams hiring internationally should plan the immigration path before they promise a start date.

The third challenge is tax and entity design. Business Sweden’s 2026 corporate tax guide states that Sweden’s corporate income tax rate is 20.6%, and Verksamt notes simplifications to the 3:12 rules for qualified shares in closely held companies from the 2026 tax year. Founders should get local tax advice before designing equity, dividends, minority employee shares, or holding structures.

The fourth challenge is differentiation. Swedish product culture is strong, so a clean interface alone will not stand out. The product needs a defensible wedge: proprietary workflow insight, distribution, regulated trust, integration depth, strong data advantage, or a painful buyer problem competitors cannot solve with a quick feature copy.

The fifth challenge is validation discipline. Swedish buyers may be willing to test new products, but a polite pilot is not product-market fit. Treat every pilot as a learning contract: what will change, what will be measured, who owns the decision, and what happens if the product works.

What European founders should build first

Founders entering Sweden should build the proof layer before the expansion layer.

For fintech, build compliance, permissions, reconciliation, risk controls, and partner trust into the product from the beginning. Sweden fintech buyers do not need another stylish payment story. They need a system that handles money, identity, fraud, and regulation without creating hidden risk.

For AI, choose a narrow workflow where output quality can be reviewed. The product should show what the model used, what it changed, what a human approved, and how errors are caught. This matters commercially as much as legally.

For climate tech, prove deployment economics. If the product touches hardware, energy, buildings, logistics, or reporting, buyers will expect a payback model and operational evidence. For climate SaaS, the product should connect reporting to action.

For SaaS, validate retention before expanding the sales motion. A Swedish design partner is useful only if the product becomes part of a repeatable workflow. Measure activation, repeat usage, team invites, feature depth, and expansion intent before assuming the market is ready.

For legal tech and professional services automation, build trust into the interface. Lawyers, accountants, and regulated teams need speed, but not at the cost of traceability, confidentiality, or professional judgment.

The founder takeaway

The Sweden startup ecosystem is strongest for founders who combine global ambition with product discipline. Stockholm gives access to capital, experienced operators, fintech history, AI momentum, SaaS talent, and a culture that values clean execution. Sweden’s climate, legal, health, and industrial opportunities add depth beyond consumer software.

The harder truth is that Swedish product culture raises the bar. Buyers and investors will not be impressed by a thin MVP dressed in clean UI. They will look for evidence that the product solves a real workflow, reduces risk, and can travel beyond the first pilot.

Build the smallest serious product, not the smallest possible demo. In Sweden, that difference matters.