Switzerland’s startup ecosystem is strongest where trust is part of the product, not an afterthought.

That makes the country unusually relevant for fintech, healthtech, AI, enterprise SaaS, robotics, medtech, and pharma-adjacent software. Swiss buyers, regulators, universities, and investors tend to reward products that can handle sensitive data, regulated workflows, technical evidence, and long enterprise adoption cycles. The tradeoff is clear: founders get access to deep research, wealthy customers, and global credibility, but they have to build for compliance, procurement, and reliability earlier than they might in faster, lighter software markets.

The practical read is this: Switzerland is not the easiest place to validate a thin SaaS idea. It is a very good place to build a serious product for customers who care about risk.

If your expansion question is more industrial, manufacturing, or DACH go-to-market focused, compare this with the Germany startup ecosystem guide before choosing the first European wedge.

For founders comparing nearby European launch paths, the Netherlands startup ecosystem guide is useful when fintech, logistics, climate, AI, or B2B SaaS buyers are more relevant than Swiss regulated-enterprise trust.

Switzerland startup ecosystem in 2026: the useful read

The Switzerland startup ecosystem has moved back into growth, but the recovery is selective. EY’s 2026 Start-up Barometer recorded 515 Swiss funding rounds in 2025 and CHF 3.3 billion in financing volume, a 44% increase in volume from 2024. AI-based startups were involved in 32% of those rounds, and AI funding rose to about CHF 1.1 billion.

The same EY data shows why the ecosystem should be read through a sector lens. Healthcare remained the largest category by capital, with about CHF 1.5 billion and 44% of total Swiss startup financing volume in 2025. Software and analytics followed at CHF 924 million, while fintech and insurtech represented 9% of volume.

This is not a broad consumer-app boom. Switzerland is becoming more attractive for products with a hard trust requirement: clinical workflow software, regulated fintech rails, AI governance, legal AI, manufacturing analytics, secure developer infrastructure, privacy systems, digital health devices, and TechBio platforms that connect AI with biology.

The deeper structural signal is even stronger. Deep Tech Nation Switzerland reports that Switzerland ranks first globally for the share of venture capital going into deep tech, at 63% across 2020 to 2026. It also reports $1,470 invested per person, record Swiss deep tech funding of $2.6 billion in 2025, and a late-stage dependence on foreign capital, with international investors supplying 88% of rounds above $100 million.

That creates a useful founder lesson. Early Swiss validation can be powerful because the ecosystem is credible, technical, and close to regulated buyers. Scaling still requires a capital and go-to-market plan that reaches beyond Switzerland.

Zurich, Lausanne, Geneva, and Basel are different markets

Switzerland is compact, but its startup hubs are not interchangeable. Founders should choose a Swiss base around customers, research anchors, hiring needs, and regulatory exposure rather than city rankings alone.

Dealroom’s Switzerland profile lists Zurich, Basel, Geneva, and Lausanne as the largest Swiss hubs by combined startup enterprise value, with Zurich at $58.3 billion, Basel at $44.6 billion, Geneva at $24 billion, and Lausanne at $21.1 billion. It also shows Switzerland’s academic flywheel: 1,805 university spinouts, 2,962 alumni-founded companies, and 238 university-linked scaleups that have raised more than $100 million.

Zurich: AI, fintech, robotics, and enterprise software

Zurich is the most natural landing zone for many Swiss startups because it combines ETH Zurich, global technology R&D centers, finance, and enterprise customers. It is particularly relevant for AI tooling, legaltech, fintech infrastructure, robotics, cybersecurity, developer tools, and B2B SaaS products that need technical credibility.

For software founders, Zurich’s advantage is not just talent. It is buyer fit. A product that improves legal review, manufacturing analytics, AI model governance, private banking operations, procurement, or engineering workflow can find design partners that understand why reliability and documentation matter.

Lausanne: EPFL-led AI, medtech, robotics, and advanced engineering

Lausanne is smaller than Zurich but unusually dense in technical output. EPFL anchors a cluster that is strong in AI, robotics, medtech, digital health, advanced materials, 3D printing, and biology-adjacent engineering. For founders commercializing research, Lausanne is useful when the product needs close proximity to technical talent, university labs, hospitals, and applied research partners.

The product implication is important: Lausanne is a strong place for products where the prototype needs scientific credibility before the sales motion scales. That includes medtech devices, diagnostics workflow software, AI-for-biology tooling, and high-precision hardware-software products.

Geneva: privacy, diplomacy, blockchain, and global institutions

Geneva’s startup opportunity is shaped by international organizations, private banking, CERN, commodity trading, global NGOs, and cross-border collaboration. It is a natural fit for privacy infrastructure, secure collaboration, blockchain and digital asset systems, sustainability software, global health tools, and enterprise software serving institutions with complex governance.

Geneva is also a useful reminder that Swiss SaaS opportunities are not only Zurich fintech or Basel biotech. Some of the most defensible products emerge where neutrality, security, multilingual operations, and global compliance are part of the buyer’s problem.

Basel: biotech, pharma-adjacent products, and TechBio

Basel is the clearest life sciences cluster. The Basel Area Life Sciences Supercluster describes the region as home to 33,000+ life sciences specialists and 800+ life sciences companies, with major anchors including Roche, Novartis, Bayer, and Moderna.

For software and AI founders, Basel matters because pharma-adjacent products have a different commercialization path from normal SaaS. A product might start as clinical data infrastructure, lab automation, regulatory workflow software, trial operations tooling, molecular design infrastructure, or AI-assisted research support. The buyer may not be a self-serve user. It may be a pharma team, research institute, hospital, regulatory function, or venture-backed biotech company that needs evidence before expansion.

Active sectors: where Swiss startups have an edge

Switzerland’s strongest sectors share a pattern: high technical depth, high trust requirements, and customers willing to pay for reliability.

AI is now threaded through most of the ecosystem. The strongest Swiss AI startups are less likely to be generic chat interfaces and more likely to be applied systems for legal search, manufacturing quality, life sciences discovery, compliance, robotics, or enterprise decision support. This fits the country’s research base and its enterprise customer profile.

Healthtech and medtech are equally important. Switzerland has the hospitals, medtech talent, precision engineering base, and regulatory exposure to support serious healthcare products. But the bar is high: clinical workflows, patient safety, medical-device classification, data protection, and reimbursement assumptions all affect the product roadmap.

Fintech remains a Swiss strength, especially around private banking infrastructure, digital assets, custody, payments, wealth operations, and compliance automation. Switzerland’s crypto and DLT history gives Zug, Zurich, and Geneva a durable role in regulated digital asset infrastructure.

Enterprise SaaS is strongest when it is vertical, technical, and workflow-specific. Deep Tech Nation’s technical enterprise software profile describes Swiss technical enterprise software as a sector with 65+ VC-backed startups and $13.7 billion in combined enterprise value. The examples are not lightweight productivity tools; they include security, developer infrastructure, digital experience management, privacy, procurement, and data systems.

TechBio is where the Swiss story becomes especially distinctive. Deep Tech Nation counts 55+ VC-backed TechBio startups, $732 million in funding since 2019, and $4.1 billion in combined enterprise value. The reason is simple: Switzerland combines ETH Zurich and EPFL engineering talent with Roche and Novartis domain gravity.

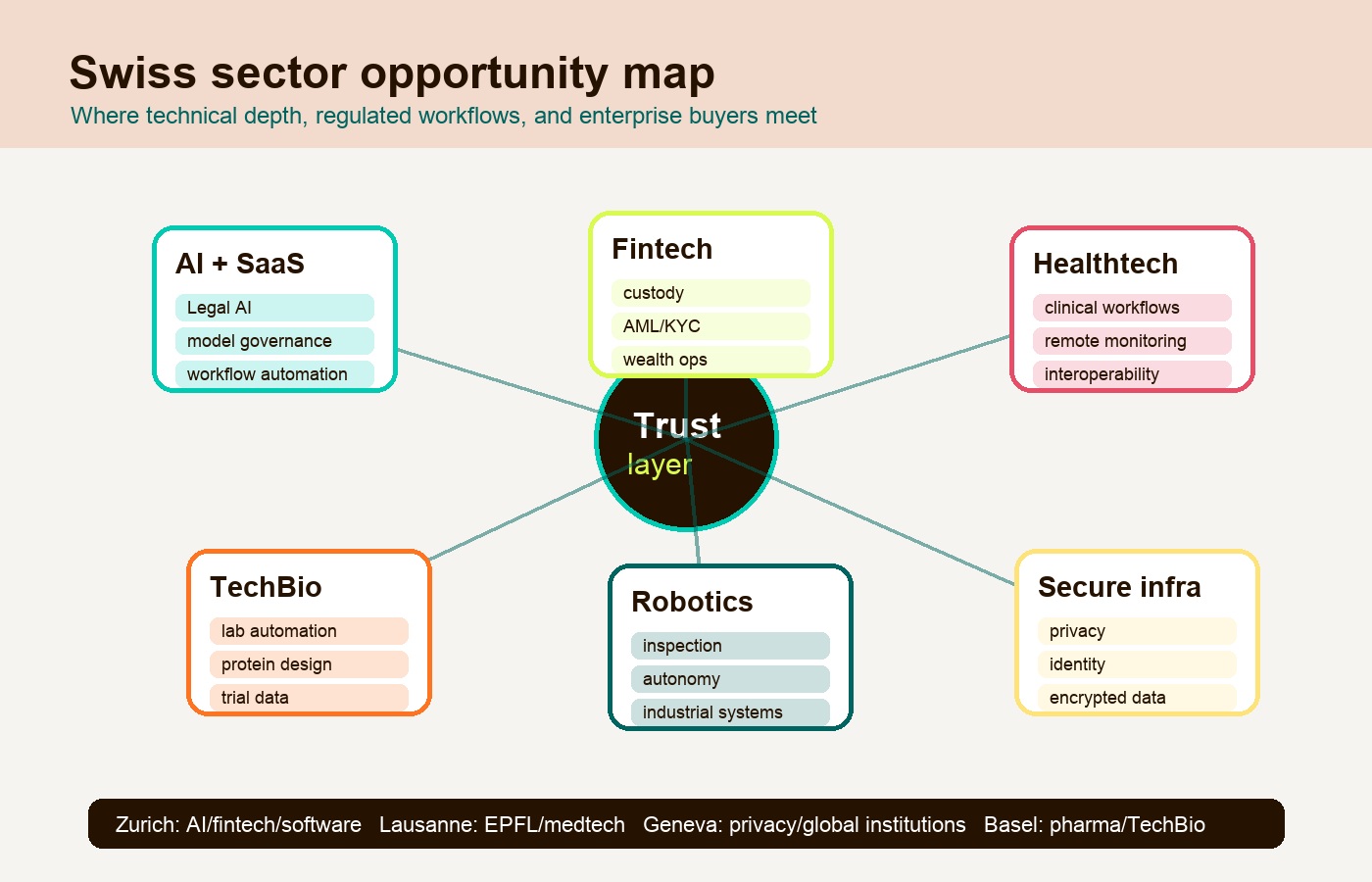

Sector opportunity matrix for founders

Use this matrix to choose a Swiss product wedge. The goal is not to chase every sector. It is to match the product’s trust requirement with the Swiss hub, buyer, and regulatory path that can turn that requirement into an advantage.

| Sector | Best Swiss wedge | Leading hubs | Product opportunities | Trust requirements |

|---|---|---|---|---|

| AI and enterprise SaaS | Workflow-specific AI for high-risk business processes | Zurich, Lausanne, Geneva | Legal AI, procurement intelligence, model evaluation, manufacturing analytics, developer tooling, data governance | Data protection, audit logs, explainability, human review, security evidence |

| Fintech and digital assets | Regulated infrastructure rather than consumer hype | Zurich, Zug, Geneva | Custody tooling, KYC/AML workflows, wealth operations, stablecoin controls, reporting automation | FINMA path, AML controls, segregation of assets, operational resilience |

| Healthtech and medtech | Clinical-grade software and connected devices | Lausanne, Zurich, Basel, Geneva | Remote monitoring, diagnostic workflows, surgical robotics, clinical data platforms, patient operations | Swissmedic path, MedDO/IvDO fit, clinical evidence, privacy, interoperability |

| TechBio and pharma-adjacent software | AI, automation, and data infrastructure for biology | Basel, Lausanne, Zurich | Protein engineering tools, lab automation, trial data systems, research workflow platforms, regulatory document systems | Scientific validation, data lineage, quality systems, pharma procurement evidence |

| Robotics and industrial systems | Autonomous systems for difficult physical environments | Zurich, Lausanne, Winterthur | Inspection robots, warehouse automation, industrial perception, machine-quality monitoring | Safety, uptime, hardware support, integration with plant systems |

| Privacy and secure infrastructure | Trust as the commercial feature | Geneva, Zurich, Zug | Encrypted collaboration, identity, secure data exchange, privacy-preserving analytics | Threat model, encryption design, hosting, compliance documentation |

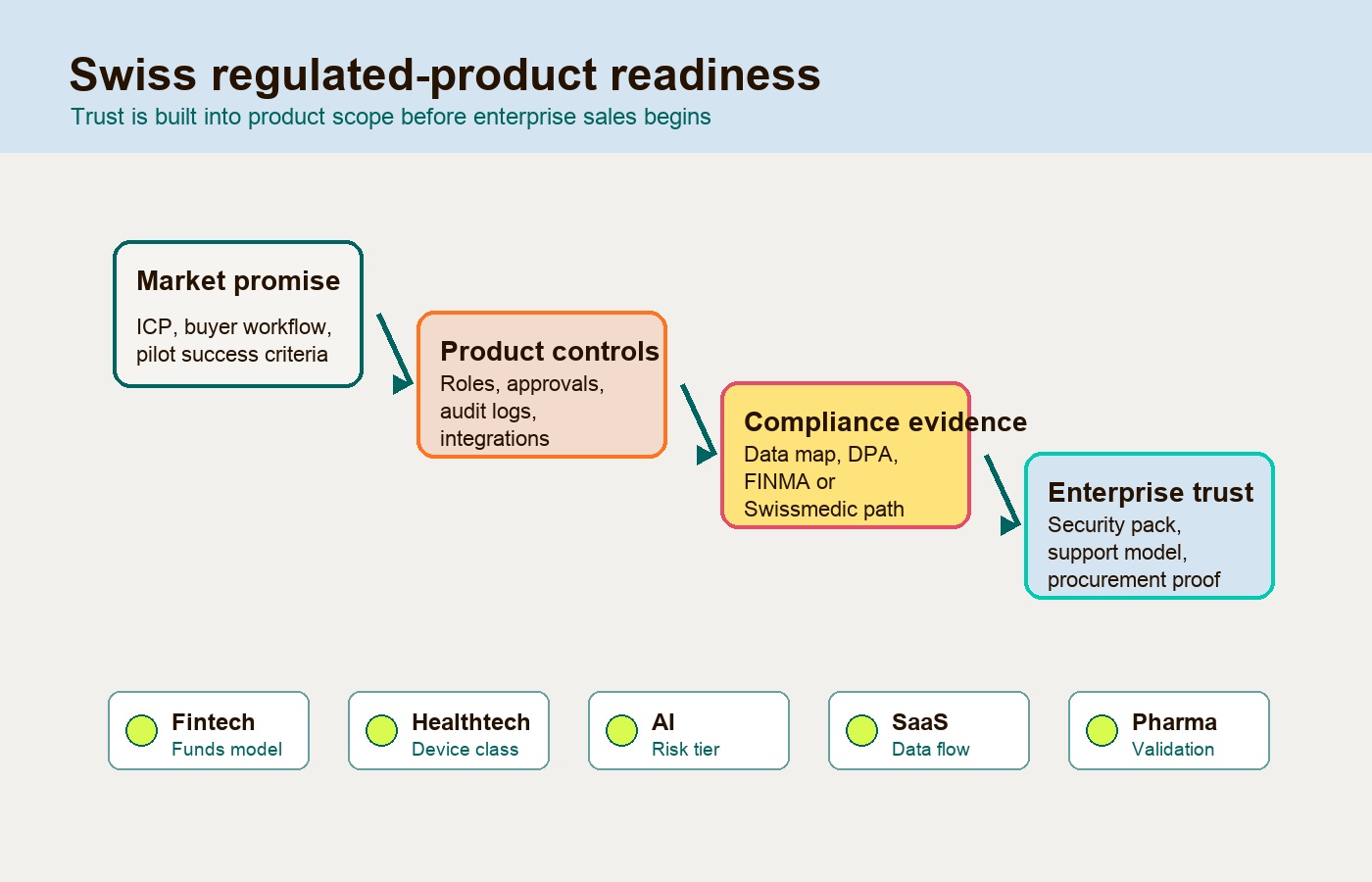

Swiss regulated-product readiness table

Swiss regulation is often principle-based, but that does not make it light. It means founders need to understand the economic and safety function of the product. If the product holds deposits, controls medical-device data, influences clinical decisions, processes sensitive personal data, or automates high-risk decisions, the compliance path becomes part of product design.

| Product type | Main authority or regime | What triggers scrutiny | Product work to prepare early |

|---|---|---|---|

| Fintech sandbox product | FINMA sandbox | Accepting public deposits up to CHF 1 million without interest or reinvestment | Deposit disclosures, AML posture, customer funds model, recordkeeping, risk notices |

| Fintech license product | FINMA fintech license | Accepting public deposits up to CHF 100 million without lending or maturity transformation | Capital model, Swiss office, governance, KYC/AML controls, operational risk management |

| Banking or securities product | FINMA banking, securities, or market infrastructure authorization | Lending, maturity transformation, securities trading, custody, or regulated market activity | Licensing strategy, compliance officer role, auditability, liquidity/risk processes, legal review |

| Medical device or IVD product | Swissmedic, MedDO, IvDO | Software or hardware placed on the Swiss market as a medical device or diagnostic | Classification, technical file, clinical evaluation, CH-REP where needed, post-market surveillance, swissdamed registration |

| AI product used in EU high-risk contexts | EU AI Act exposure for EU market use | Employment, healthcare, credit, education, critical infrastructure, biometrics, or regulated product integration | Risk management, dataset controls, logging, technical documentation, human oversight, robustness and cybersecurity |

| Enterprise SaaS handling sensitive data | Swiss FADP and GDPR exposure where EU data is involved | Personal data, employee data, health data, finance data, cross-border processing | Data map, DPA, subprocessors, retention, access controls, breach process, privacy-by-design architecture |

FINMA explains that the Swiss fintech license covers institutions accepting public deposits up to CHF 100 million without lending activity, while the sandbox allows public deposits up to CHF 1 million under defined limits and AML expectations. The Federal Office of Public Health notes that Switzerland has aligned medical-device legislation with EU MDR and IVDR, while also requiring economic-operator and product registration measures through Swissmedic from July 2026.

For AI founders, the EU AI Act matters even when the company is Swiss because many Swiss startups sell into the EU. The European Commission explains that the AI Act is risk-based, with high-risk systems requiring risk management, data quality, logging, documentation, human oversight, robustness, cybersecurity, and accuracy before market use.

Funding and venture capital: strong early, selective late

Swiss venture capital is healthier than it was during the 2022-2023 contraction, but the money is not evenly distributed. Early-stage technical companies can raise when they have credible science, a real buyer problem, and a strong founding team. Later-stage companies often still need international capital.

That late-stage gap should shape founder planning. If the company is building a regulated or deep tech product, the seed-stage milestone should not be “we built the MVP.” It should be “we produced evidence that a serious customer or regulator will respect.”

Useful proof points include:

- A design partner in a regulated industry.

- A documented workflow with acceptance criteria.

- A security and data-protection pack ready for procurement.

- A regulatory classification memo, even if the product is not yet regulated.

- Technical validation from ETH, EPFL, a hospital, pharma partner, or enterprise customer where relevant.

- Architecture that can support audit logs, permissions, data lineage, and integration without a rewrite.

This is why product discipline matters so much in Switzerland. A founder can raise attention with a strong research story. They earn enterprise traction by turning that research story into repeatable, inspectable product behavior.

Accelerators, funds, and support networks worth knowing

Switzerland has a dense support layer, but founders should choose programs based on sector fit rather than logo count.

For science-led startups, ETH Zurich, EPFL, university technology-transfer teams, Innosuisse, Venture Kick, and BaseLaunch are often more relevant than generic accelerators. Basel-based biotech founders should study BaseLaunch and Basel Area networks. Enterprise software and AI founders should look at Swisscom Ventures, Founderful, b2venture, Lakestar, Redalpine, Verve Ventures, VI Partners, and sector-specific operator networks. Fintech and crypto founders should understand Zug’s Crypto Valley network, FINMA expectations, and bank partnership paths before assuming regulation will be solved later.

The private scale-up layer is also maturing. Deep Tech Nation’s summary of the Swiss Startup Agenda points to the structural issue clearly: Switzerland is good at creating companies, but still working on the policy and capital environment for scaling. The agenda highlights ESOP standardization, faster work permits, pension fund investment, corporate venture incentives, digital government services, founder social security, and improved VC fund structures as priority reforms.

For founders, the takeaway is practical. Switzerland has high-quality help, but it is expensive to wander. Pick the support network closest to the product’s buyer, regulator, and technical proof point.

Founder challenges: the price of credibility

The Swiss startup market has three recurring founder challenges: cost, talent mobility, and scaling capital.

Costs show up early. Senior engineering talent, legal advice, accounting, office space, lab space, and Swiss operations are expensive. That does not mean founders should avoid Switzerland. It means they should be honest about what must be built locally and what can be built through distributed teams, nearshore engineering, or fractional leadership.

Talent is strong but constrained. ETH Zurich and EPFL produce exceptional founders and engineers, and Switzerland attracts global research talent. But work permits, startup visa gaps, and equity-compensation complexity can make hiring harder than the raw talent density suggests.

The third issue is capital depth. Switzerland produces premium companies, but late-stage deep tech rounds still rely heavily on foreign capital. That can be a strength if the company uses Swiss credibility to attract global investors. It becomes a weakness if the company waits too long to build an international fundraising and customer strategy.

The operating advice is simple: keep the Swiss trust advantage, but avoid building a Switzerland-only company unless the market is intentionally local.

Product opportunities worth building for

The best Swiss product opportunities are not generic “AI for X” ideas. They are products where compliance, workflow fit, and technical evidence make the buyer more confident.

In fintech, that means custody operations, compliance automation, onboarding controls, transaction monitoring, stablecoin governance, wealth operations, reporting, and secure data exchange between banks and fintechs. The product needs to respect FINMA expectations, AML obligations, and bank-grade operational resilience from the start.

In healthtech, the opportunities sit in clinical operations, remote monitoring, diagnostic workflows, data interoperability, patient follow-up, and device-connected software. The hard part is not only building the app. It is knowing whether the product is a medical device, how clinical evidence will be gathered, how patient data will be protected, and how the workflow fits clinicians rather than demo rooms.

In AI and enterprise SaaS, the opening is vertical AI with proof: legal knowledge retrieval, procurement review, manufacturing analytics, quality assurance, secure developer tooling, model evaluation, and internal workflow automation. Products should ship with permissions, logging, exception handling, and human-in-the-loop review before the first enterprise pilot.

In TechBio and pharma-adjacent software, founders can build around lab automation, protein engineering, clinical trial data flows, regulatory writing, quality systems, research data lineage, and AI-assisted discovery. The buyer will care about reproducibility and validation more than interface polish.

In robotics and compute-adjacent infrastructure, Switzerland’s engineering base supports industrial robots, inspection systems, chip cooling, sensors, and high-performance computing components. These products need field reliability, hardware support, safety evidence, and integration into physical operations.

What to build before selling to Swiss enterprise buyers

Founders entering Switzerland should treat enterprise trust as a product layer. A polished demo is useful, but it is not enough for buyers in banking, healthcare, pharma, legal, manufacturing, or public-sector-adjacent markets.

Before active sales, prepare the basics:

- Map the workflow you are improving, including exceptions, approval paths, and handoffs.

- Document data flows, data residency, subprocessors, retention, deletion, and access permissions.

- Build audit logs and role-based access before a buyer asks for them.

- Prepare security documentation, even if it is lightweight at first.

- Define acceptance criteria for pilots so success is not subjective.

- Identify regulatory triggers and write them into the roadmap.

- Plan integrations with the systems your buyer already uses.

- Decide which support expectations are local, multilingual, or enterprise-grade.

Hapy’s guide to web application architecture is useful when the product has to support auditability, scalability, and integrations. The quality assurance methodology guide is especially relevant for regulated or enterprise workflows where testing is evidence, not just bug cleanup. If the product requires custom workflows, our custom software development services buyer guide can help founders scope discovery, ownership, architecture, and post-launch responsibility before the build becomes expensive.

The founder takeaway

The Switzerland startup ecosystem rewards founders who build credible products for serious workflows. Zurich, Lausanne, Geneva, and Basel each offer different advantages, but the common thread is trust: technical trust, compliance trust, clinical trust, financial trust, and enterprise-operational trust.

For European founders and B2B founders, Switzerland is a strong place to build when the product benefits from research depth, regulated buyers, pharma or finance proximity, and a premium trust signal. It is a weaker fit for products that depend on fast, low-friction adoption without documentation, procurement evidence, or workflow depth.

Build the trust layer early. In Switzerland, that is not overhead. It is the product.