Germany’s startup ecosystem is not the easiest place to sell software, and that is exactly why serious B2B founders should study it carefully.

The opportunity is real: industrial customers, export-heavy companies, AI adoption in manufacturing, dense university spinouts, and large Mittelstand buyers that still run important workflows on fragmented systems. The catch is also real: procurement is slower, privacy expectations are stricter, German-language trust signals matter, and buyers often expect software to fit their domain workflow before they treat it as strategic.

For B2B SaaS, AI, and Industry 4.0 startups, Germany is a market where “good product” is not enough. The product has to survive local compliance, integration, documentation, procurement, and support reality. A founder entering Germany should ask a practical question before hiring a local sales team: can the product already operate inside a German buyer’s workflow without creating new risk?

If you are comparing DACH markets, pair this Germany view with the Switzerland startup ecosystem guide because Swiss fintech, healthtech, AI, and enterprise SaaS buyers often reward a different trust and compliance posture.

Germany startup ecosystem in 2026: the useful read

The Germany startup ecosystem is strong where software touches serious operational problems: industrial automation, AI tooling, enterprise software, healthtech, climate tech, logistics, fintech infrastructure, cybersecurity, and manufacturing software. It is less forgiving for thin SaaS products that rely on fast outbound, light onboarding, or generic English-only positioning.

Dealroom’s Germany profile shows why the market deserves attention. Germany is listed as Europe’s number eight startup ecosystem by enterprise value, with a public profile showing about $418 billion in startup enterprise value and a deep funnel of pre-seed, seed, Series A, Series B, unicorn, and decacorn companies. The same profile shows Germany’s university-linked startup formation as a major advantage, including more than 2,500 university spinouts and thousands of alumni-founded companies.

The capital story is improving but still selective. Startup Genome’s 2026 European report says Europe’s Series A funding grew 10% from 2024 to 2025, then Q1 2026 ran 56% above the 2025 quarterly average. The same report frames Europe’s recovery as concentrated around AI, defense, deep tech, and strategic sectors, not a broad return to low-friction consumer startup funding.

That matters for German B2B SaaS founders because the strongest buyer pain often sits inside established sectors: manufacturing, finance, logistics, healthcare, insurance, energy, public infrastructure, and professional services. Investors may like AI-native narratives, but German customers usually reward less glamorous execution: better audit trails, cleaner handoffs, reliable integrations, and fewer operational surprises.

Berlin, Munich, and Hamburg without turning this into a ranking

German startups are not concentrated in one city. Berlin, Munich, Hamburg, Stuttgart, Cologne-Bonn, Frankfurt, and the Ruhr each bring different customer networks and technical strengths. For a founder, the right question is not “which city is best?” It is “where are the customers, partners, technical hires, and proof points for this product?”

Berlin is still the most natural landing zone for many software and AI companies. It has international talent density, strong startup hiring loops, fintech and enterprise software history, and the brand recognition that helps foreign founders start conversations. Dealroom’s hub data shows Berlin-Brandenburg with the largest enterprise value among German sub-national ecosystems, while Startup Genome still treats Berlin as one of Europe’s core startup cities. For B2B product teams, Berlin is often useful for software talent, GTM hiring, investor access, fintech, AI applications, climate software, and commercial pilots with tech-forward buyers.

Munich is a different kind of advantage. It is more deeply tied to engineering, advanced manufacturing, aerospace, robotics, quantum, defense, and industrial customers. Startup Genome calls Munich a standout AI growth story, with AI-native ecosystem value rising 330% since GSER 2024 to $6.2 billion. TUM and UnternehmerTUM are central to that story: TUM reported in February 2026 that UnternehmerTUM was named Europe’s leading startup hub by the Financial Times for the third consecutive year. For industrial AI and deep tech founders, Munich can offer something Berlin cannot always replicate: tight proximity to research, engineering talent, manufacturing customers, and corporate venture-client models.

Hamburg has a clearer logistics, maritime, media, and green technology profile. The Hamburg Startup Monitor 2026 reported 1,540 active startups, 203 new startups founded in 2025, and 22% of Hamburg startups in GreenTech. It also shows the city’s scaleup capital gap: since 2015, Hamburg startups have attracted 3.3 billion euros, compared with 38 billion euros in Berlin and 12 billion euros in Munich. For founders, that does not make Hamburg weaker. It means the product strategy should be specific: logistics software, port and maritime operations, sustainability reporting, industrial supply chains, and B2B products that benefit from local corporate relationships.

What the funding trend actually means for founders

Germany venture capital is available, but it is not patient with vague positioning. The 2026 market favors startups that can show why their product belongs in a strategic budget line: AI that improves a workflow, software that reduces compliance or operating cost, deep tech with credible commercialization paths, or infrastructure that helps large companies modernize without breaking trust.

Founders should read that as a product requirement, not only a fundraising signal. If the deck says “AI for manufacturing” but the product cannot handle plant-level permissions, production data constraints, audit logs, edge deployment questions, and integration with existing MES or ERP workflows, German buyers will see the gap quickly.

The federal support environment also points in the same direction. The EXIST Startup Factories program says ten Startup Factories entered the project phase in 2025, built as public-private partnerships across 126 universities and research institutions and 144 business partners, with around 110 million euros in private financing. These initiatives are designed to increase knowledge-based deep tech spinouts, not produce another wave of generic SaaS landing pages.

For founders, the best use of this ecosystem is practical:

- Use Berlin for software, AI, fintech, product talent, and international hiring.

- Use Munich for deep tech, industrial customers, aerospace, robotics, AI infrastructure, and university-commercialization networks.

- Use Hamburg for logistics, maritime, green tech, media, and supply-chain workflows.

- Use Stuttgart, Baden-Wurttemberg, and the Ruhr when the product needs automotive, robotics, advanced manufacturing, materials, or industrial transformation customers.

Where Germany AI startups and Industry 4.0 meet

Germany AI startups are strongest when AI is attached to a domain-specific workflow. That is a better commercial story than selling “AI” as a feature label.

The appliedAI Institute’s German AI Startup Landscape 2025 counted 935 German AI startups, up 36% from the previous year. The report also notes a strict inclusion logic: startups need a credible business model, team capacity, and internal AI competence. That distinction matters because German enterprise buyers are becoming more skeptical of AI branding without technical depth.

Industry 4.0 gives AI startups a real demand surface. Germany Trade & Invest, citing a Bitkom survey of 555 manufacturing companies with at least 100 employees, reported in April 2026 that 97% of industrial companies use at least one Industrie 4.0 application, 81% consider it very important or indispensable to international competitiveness, 40% already use AI for intelligent control and planning, and 45% use digital twins.

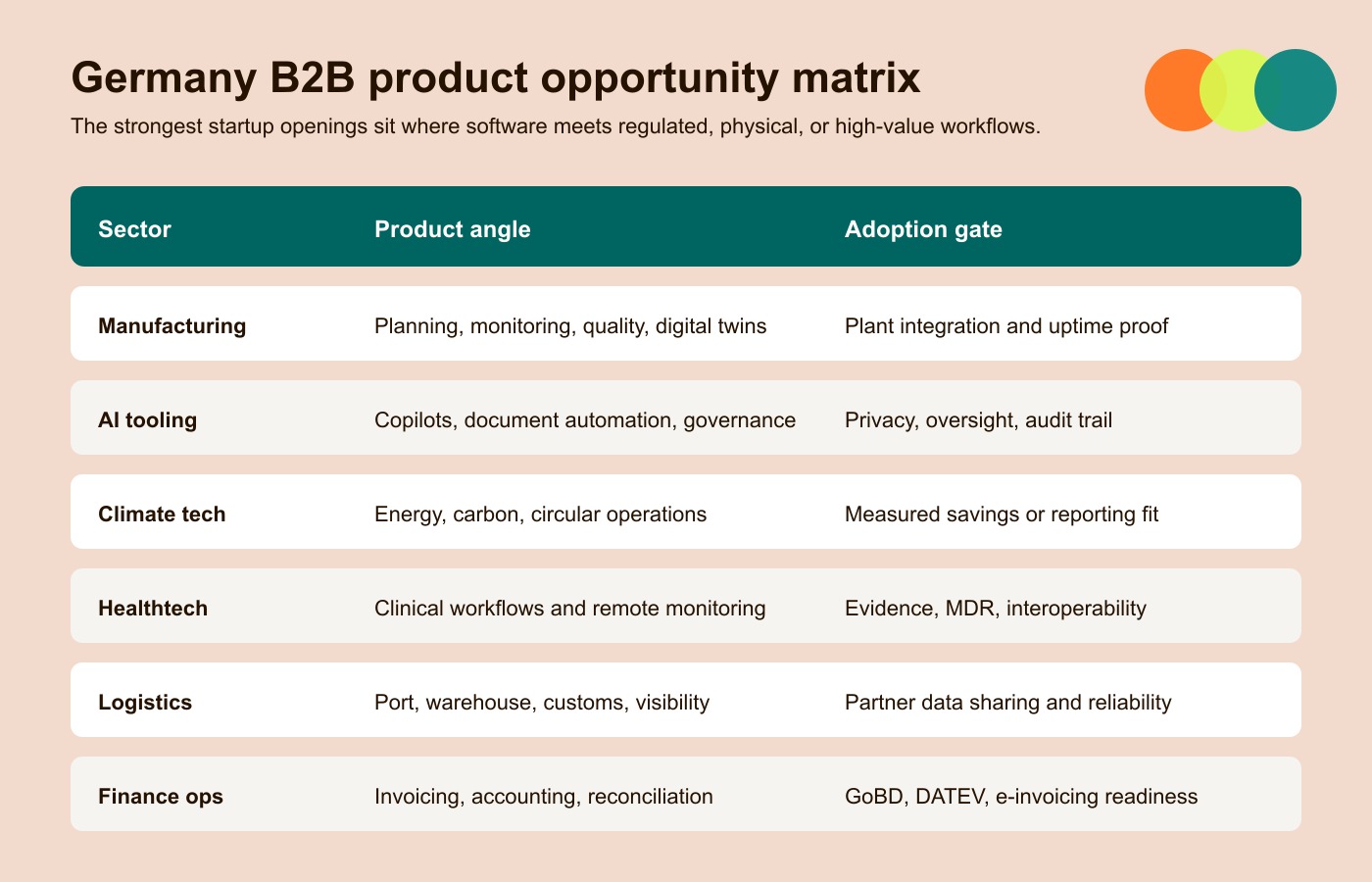

That creates product opportunities in places where software improves physical operations:

| Sector | Strong startup angle | What German buyers will test |

|---|---|---|

| Manufacturing software | Production planning, machine monitoring, predictive maintenance, quality inspection, digital twins | Integration with plant systems, uptime, auditability, on-prem or edge options, operator workflows |

| AI tooling | Domain copilots, document automation, data extraction, workflow orchestration, model governance | Data protection, human oversight, explainability, permissions, procurement security evidence |

| Climate tech | Energy optimization, carbon accounting, grid flexibility, industrial efficiency, circularity | Measurable savings, regulatory reporting fit, hardware dependency, payback period |

| Healthtech | Clinical workflow software, remote monitoring, patient engagement, medical operations | MDR class, reimbursement path, data hosting, clinical evidence, interoperability |

| Logistics and maritime | Route optimization, customs workflows, port operations, supply-chain visibility | Reliability, ERP/TMS integration, multilingual operations, data sharing across partners |

| Fintech and finance ops | Compliance automation, invoicing, accounting, reconciliation, treasury workflows | BaFin-adjacent risk, GoBD, DATEV export, audit trails, e-invoicing readiness |

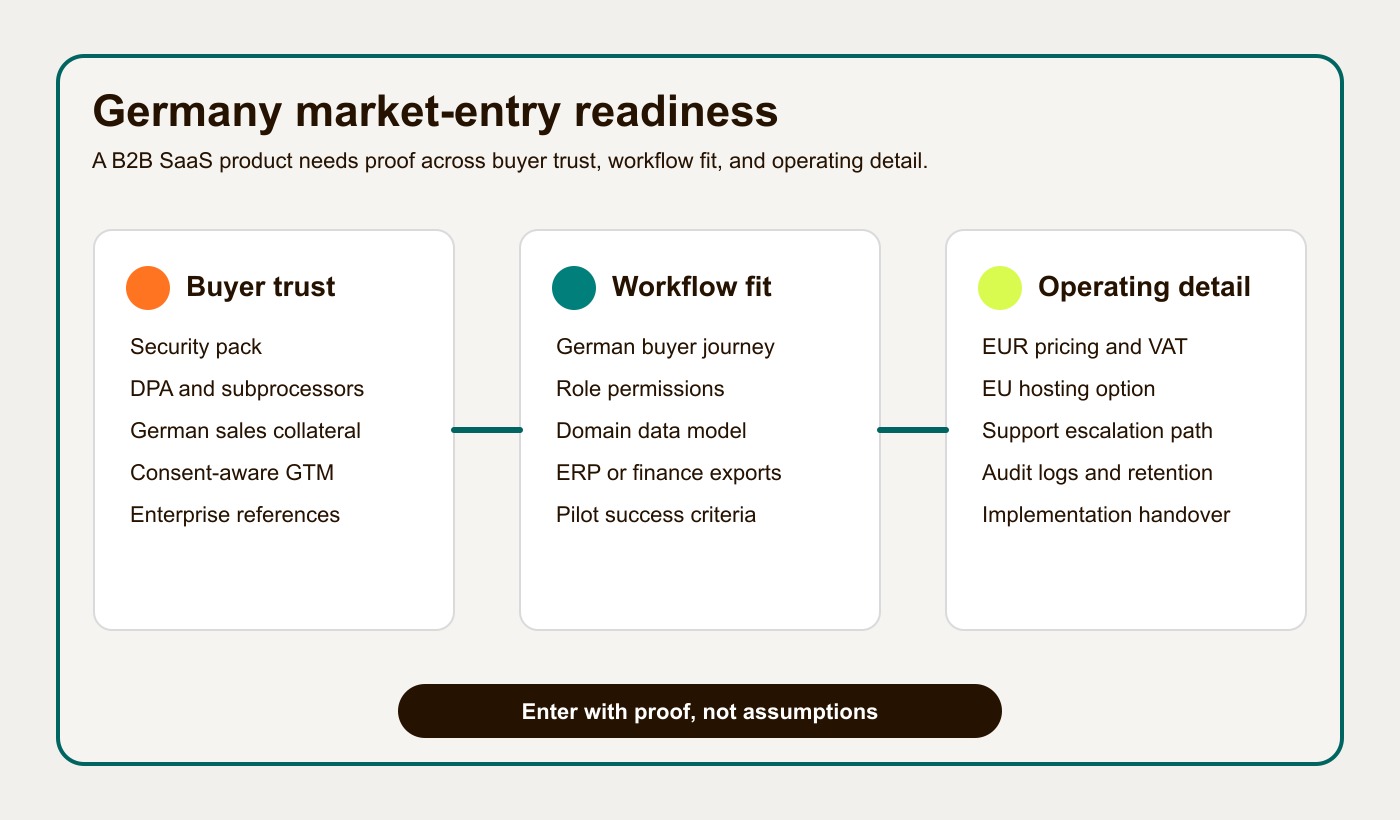

The German B2B SaaS localization checklist

German B2B SaaS localization is not just translation. It is the work of making the product feel legally, operationally, and commercially usable for a German customer.

Use this checklist before treating Germany as an active sales market:

| Area | Minimum readiness standard |

|---|---|

| Language | German website pages for buyer intent, product docs for admins, sales collateral, onboarding emails, and support macros |

| Procurement | Security pack, DPA, subprocessors list, hosting location, SLA, insurance evidence, accessibility notes, and clear order forms |

| Privacy and consent | GDPR-ready data map, cookie/tracking controls, no sloppy enrichment, and consent records for marketing channels |

| Outbound sales | Avoid unsolicited commercial email without consent; Germany’s UWG Section 7 is stricter than many SaaS teams expect |

| Finance workflows | German VAT handling, invoice fields, e-invoicing roadmap, audit logs, and DATEV export if touching accounting or expenses |

| Support | German-language support path, local working-hour expectations, escalation rules, and customer success material |

| Product UX | Local date, number, address, tax, currency, and legal notice conventions where relevant |

| Integrations | ERP, CRM, accounting, identity, and data warehouse connectors that match the buyer’s operating stack |

| Hosting and security | EU hosting option, data residency clarity, role-based access, logs, backups, retention settings, and incident process |

| Implementation | Clear discovery, workflow mapping, pilot plan, acceptance criteria, and documented handover |

This is where many international SaaS teams misread the market. They translate the homepage, hire one DACH seller, and assume the product is localized. German buyers often need deeper proof: the product can handle the workflow, the vendor can handle the compliance conversation, and the team will not disappear after the pilot.

If a product still has unclear workflows, weak acceptance criteria, or fragile architecture, fix that before entering Germany. Hapy’s guides to software requirements specification and web application architecture are useful starting points for tightening the product before sales pressure exposes gaps.

Procurement and privacy are product constraints

Germany’s procurement culture can frustrate founders used to faster markets. Enterprise buyers often expect more proof before they start, more documentation before legal review, and more confidence that the vendor understands local risk. This slows early sales but can improve retention once the product is embedded.

Privacy and outbound rules are part of that trust equation. GDPR is the baseline, but German electronic marketing rules are also shaped by the Unfair Competition Act. In practical terms, a B2B SaaS company should not assume that scraped lists plus cold email sequences are safe. Build a consent-aware GTM motion around targeted LinkedIn, events, partner referrals, content, webinars, warm intros, and direct sales conversations where permission to send follow-up material is captured.

Finance and admin workflows need similar care. If the software touches accounting, invoicing, expenses, procurement, or ERP records, German customers will ask about GoBD, audit trails, immutability, export formats, and tax-advisor workflows. DATEV compatibility can become a buying requirement because many German accountants and tax advisors work inside the DATEV ecosystem. B2B e-invoicing is also moving into the core operating stack, so products that generate or process invoices need a roadmap for structured invoices, not just PDF attachments.

The lesson is simple: in Germany, compliance details are not after-sales paperwork. They shape the product scope.

Founder challenges in Germany

The founder pain points are familiar but sharper in Germany: bureaucracy, slower public administration, conservative procurement, fewer late-stage funding options than the U.S., and a fragmented European go-to-market path. The German Startup Monitor 2025, summarized by Munich Startup, reported concern around capital access, bureaucracy, and the fact that more founders are questioning whether they would start again under current conditions.

International founders should also remember that Germany is not one homogeneous market. A Berlin fintech pilot, a Munich industrial AI deployment, a Hamburg logistics workflow, and a Baden-Wurttemberg manufacturing integration can have very different stakeholders, risk thresholds, and proof requirements.

That can feel heavy, but it creates a moat for founders who do the work. If your product fits the workflow, speaks the buyer’s language, handles privacy and procurement cleanly, and integrates into the existing stack, competitors cannot copy that trust overnight.

German market-entry readiness table

Use this table as a pre-launch scorecard. A “yes” should mean evidence exists, not only that the team plans to do it later.

| Readiness area | Not ready | Ready enough to test | Strong Germany fit |

|---|---|---|---|

| Customer segment | Broad DACH target with no named workflow | 10-20 target accounts by sector and role | Clear ICP with German buyer pains, budget owner, and internal champion |

| Product workflow | Generic SaaS flow | Localized admin and buyer journey | Domain workflow mapped to German operations, approvals, and exception cases |

| Compliance | Generic GDPR page | DPA, subprocessors, data map, consent posture | Procurement-ready security, privacy, audit, and regulatory evidence |

| Localization | English-only product and sales | German sales collateral and support path | German docs, onboarding, legal notices, product copy, and support coverage |

| Integrations | API exists but no local stack proof | CRM/ERP/accounting integration plan | Tested integrations with likely German systems and export formats |

| Pricing and contracting | USD-only, self-serve only | EUR pricing and enterprise order form | Local procurement terms, invoicing flow, VAT handling, and pilot-to-contract path |

| GTM motion | Cold outbound first | Partner, event, content, and targeted sales motion | Consent-aware pipeline with references, local champions, and repeatable proof |

| Implementation | Product demo only | Pilot plan with success criteria | Discovery, requirements, rollout plan, training, support, and ownership model |

If most rows sit in the first column, Germany is probably too early. If most rows sit in the middle, run focused pilots. If several rows reach the third column, the market can become a defensible expansion path.

Product opportunities worth building for

The strongest Germany opportunities are not generic “AI SaaS” ideas. They are products that reduce real operating friction for buyers with high process complexity.

- Manufacturing intelligence that connects machine data, quality events, maintenance, and production planning without demanding a rip-and-replace project.

- AI workflow tools that help teams review technical documents, RFQs, contracts, compliance evidence, or support tickets with human oversight and traceable decisions.

- Finance operations software that respects German invoice, audit, export, and tax-advisor workflows from the start.

- Climate and energy software that can prove savings or compliance impact, not only reporting polish.

- Healthtech and care software that understands MDR, reimbursement, clinical evidence, patient privacy, and operational adoption.

- Logistics software for port, maritime, customs, warehouse, and cross-border supply-chain workflows.

- Security and governance products for AI adoption, especially where EU AI Act obligations affect documentation, monitoring, and human oversight.

The EU AI Act is especially relevant for AI founders. The European Commission explains that the AI Act entered into force on August 1, 2024, with prohibited practices and AI literacy obligations applying from February 2, 2025, GPAI obligations applying from August 2, 2025, and staged high-risk obligations following later timelines, including rules for certain high-risk areas from December 2, 2027. If your product touches employment, health, critical infrastructure, biometrics, education, credit, or public services, build the compliance workflow early instead of retrofitting it after enterprise review.

What founders should do before entering Germany

Do not start with a city ranking. Start with a product-readiness audit.

Pick one narrow sector, one buyer role, and one operational workflow. Interview German buyers before localizing the entire product. Translate only the assets that matter for trust and conversion. Build a procurement pack before the first serious enterprise call. Map privacy, support, hosting, invoicing, and integration questions into the product backlog. Then run pilots where the success criteria are visible to both the buyer and your team.

If you are building a new product for the Germany startup ecosystem, treat localization as part of product development, not as a marketing task. For custom workflows, the planning discipline matters as much as the code; Hapy’s custom software development services buyer guide can help teams think through discovery, ownership, scope, architecture, and post-launch responsibility before a build becomes expensive.

Germany rewards founders who respect the details. It is not the fastest B2B SaaS market, but it can be one of the most defensible when the product solves a real operational problem, fits local workflows, and earns trust through evidence.